Prices keep rising because this spring’s inventory is lower than usual. The sliver of good news for buyers is that mortgage rates have declined slightly.

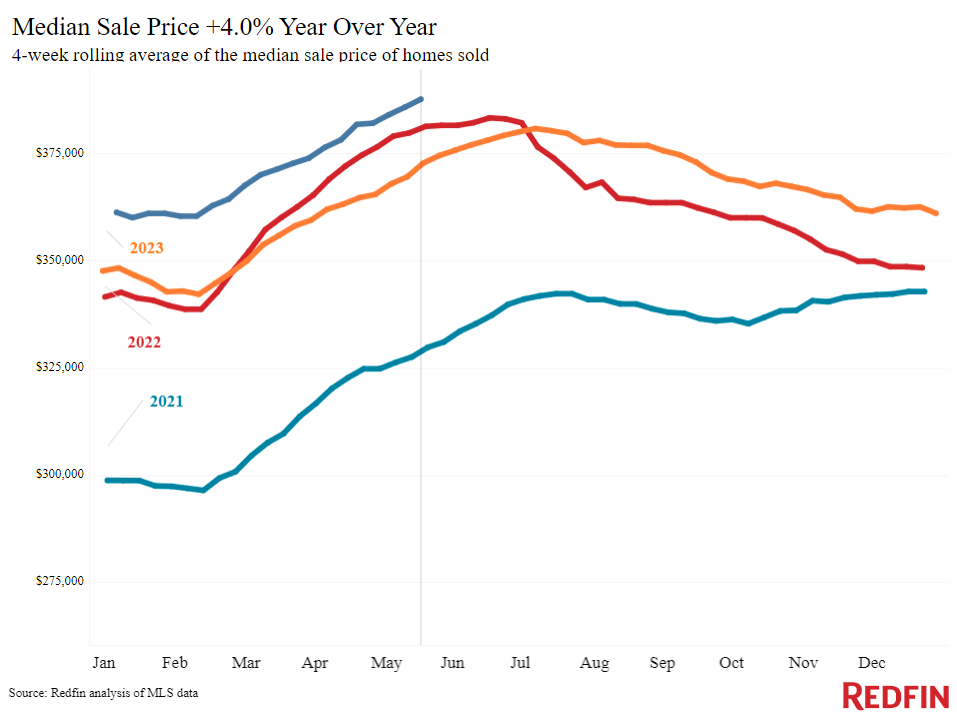

The median U.S. home-sale price hit a record $387,600 during the four weeks ending May 19, up 4% from a year earlier. Weekly average mortgage rates dipped to 7.02% from a five-month high of 7.22% at the start of the month, bringing the median monthly housing payment to $2,854, roughly $20 shy of April’s all-time high.

High housing costs pushed pending home sales down 4.2% year over year, the biggest decline in three months (except the prior 4-week period, when sales declined 4.4%). Prices keep rising despite declining sales because there aren’t enough homes on the market: New listings are up about 8% year over year, but inventory remains lower than typical spring levels. Many homeowners are staying put because they would rather hold onto their relatively low mortgage rate than move up to a bigger and/or better home.

“Move-up buyers feel stuck because they’re ready for their next house, but it just doesn’t make financial sense to sell with current interest rates so high,” said Sam Brinton, a Redfin Premier agent in Salt Lake City, UT. “The homeowners listing right now are often doing so because they need to: One of my clients is selling because of a family emergency, and another couple is selling because they had a baby and simply don’t have enough room. Buyers should take note that many of today’s sellers are motivated; if a home doesn’t have other offers on the table, offer under asking price and/or ask for concessions because many sellers are willing to negotiate.”

For Redfin economists’ takes on the housing market, including how current financial events are impacting mortgage rates, please visit Redfin’s “From Our Economists” page.

Refer to our metrics definition page for explanations of all the metrics used in this report.