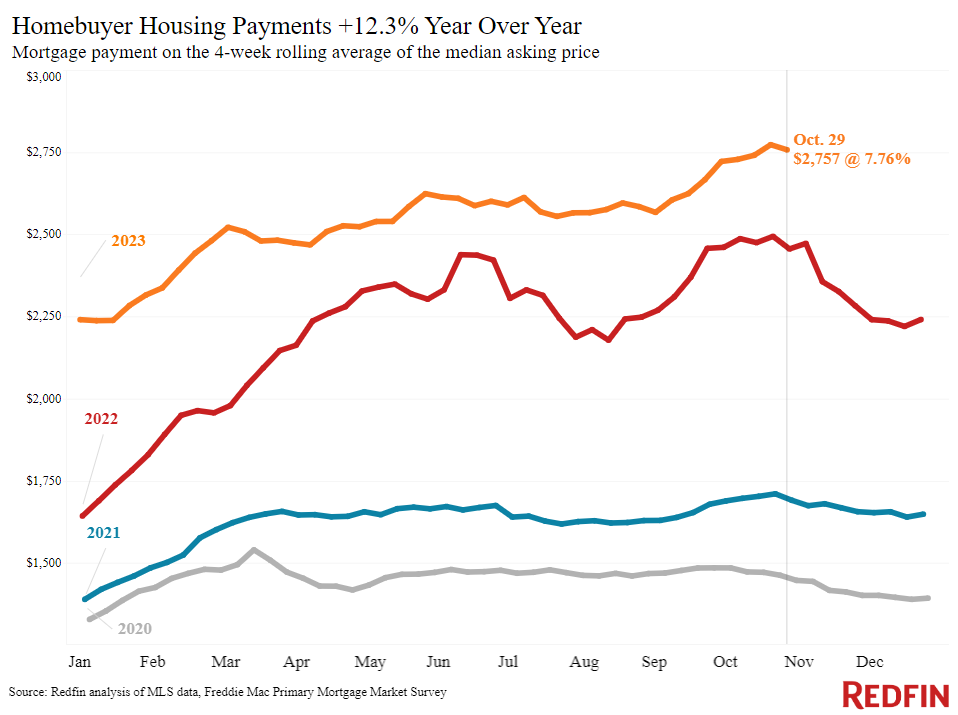

Budgets are getting some relief right now, with daily average rates dropping considerably from 8% to 7.5% over the last week.

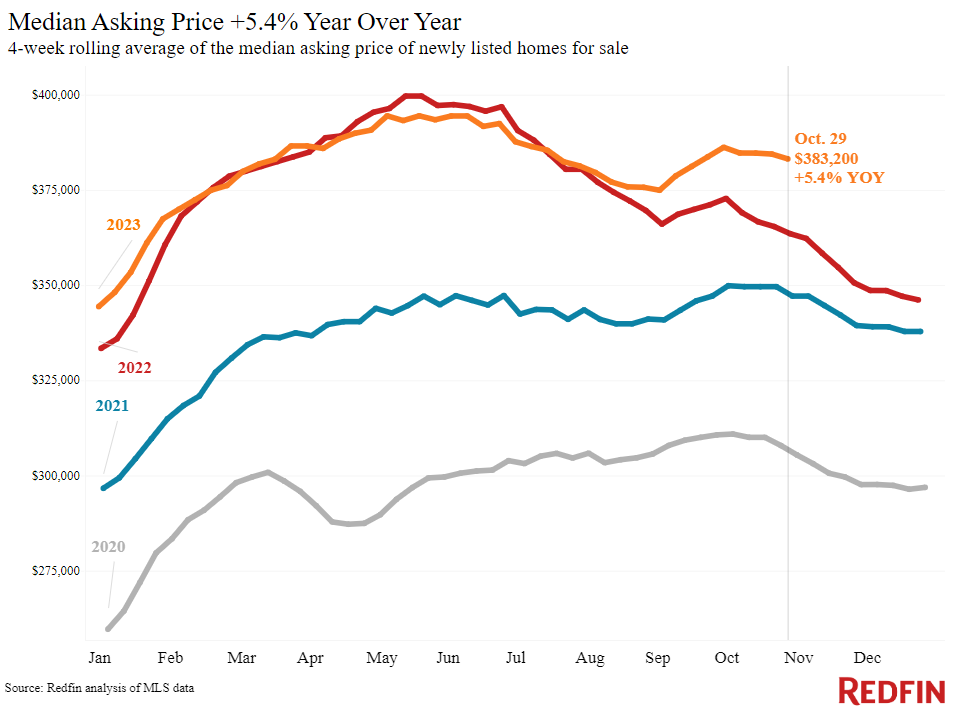

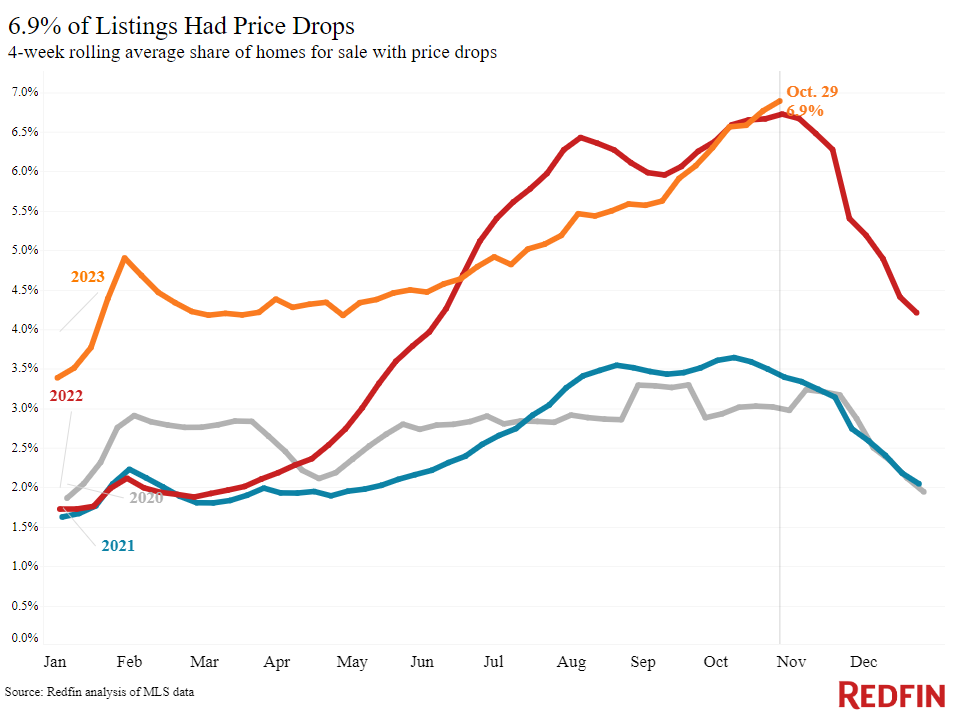

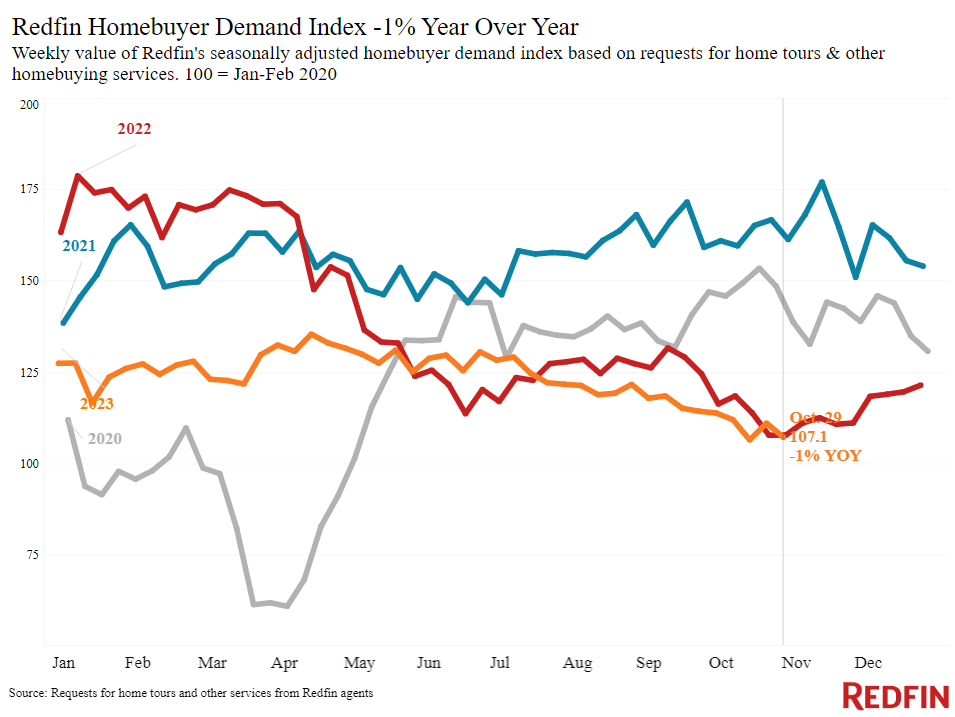

Nearly 7% of for-sale homes posted a price drop during the four weeks ending October 29, on average, the highest portion on record. The record comes as mortgage rates hover at elevated levels, hitting their highest level in 23 years last week and cutting deep into buyers’ budgets. High rates have forced some sellers to lower their asking price to make up for high interest rates on monthly payments. It’s worth noting that buyers are getting a bit of relief this week, at least temporarily: Economic events sent daily average mortgage rates from 8% down to 7.5% over the last week.

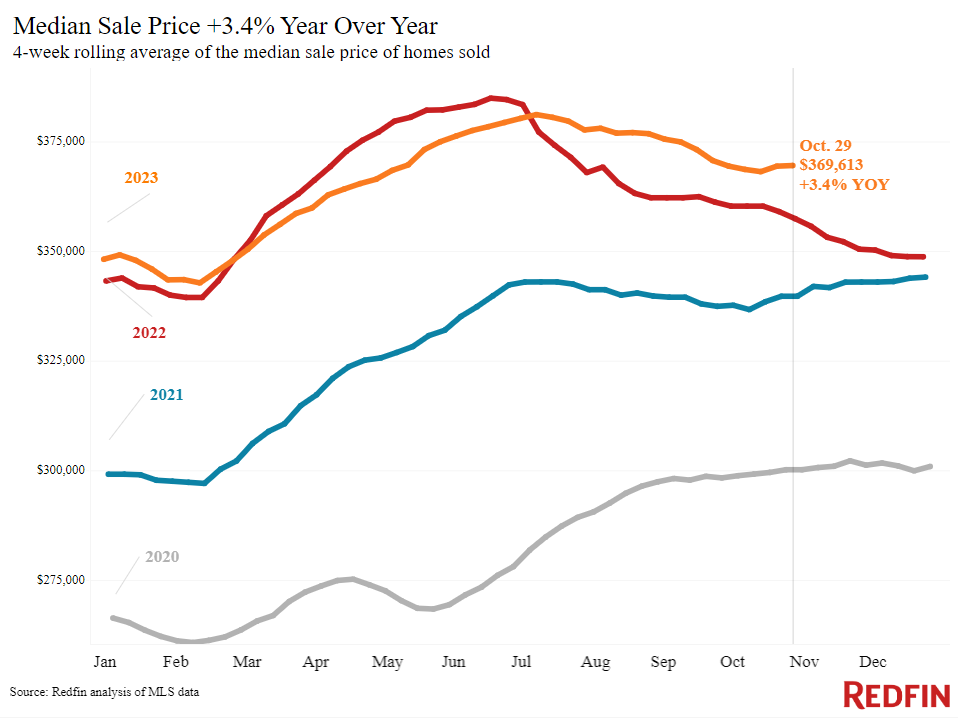

Sale prices are still up 3% from a year ago. That’s partly because sale-price data is a lagging indicator, reflecting deals that went under contract a month or two ago. Growth in sale prices may slow in the coming months as it starts to reflect sales that went under contract as mortgage rates hit 8% in October.

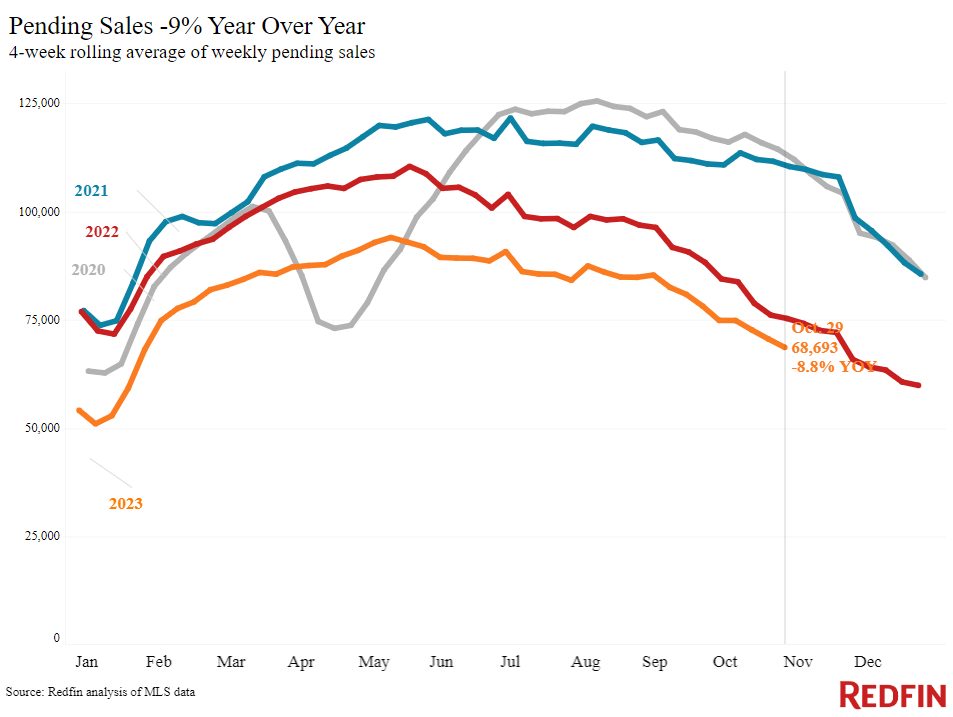

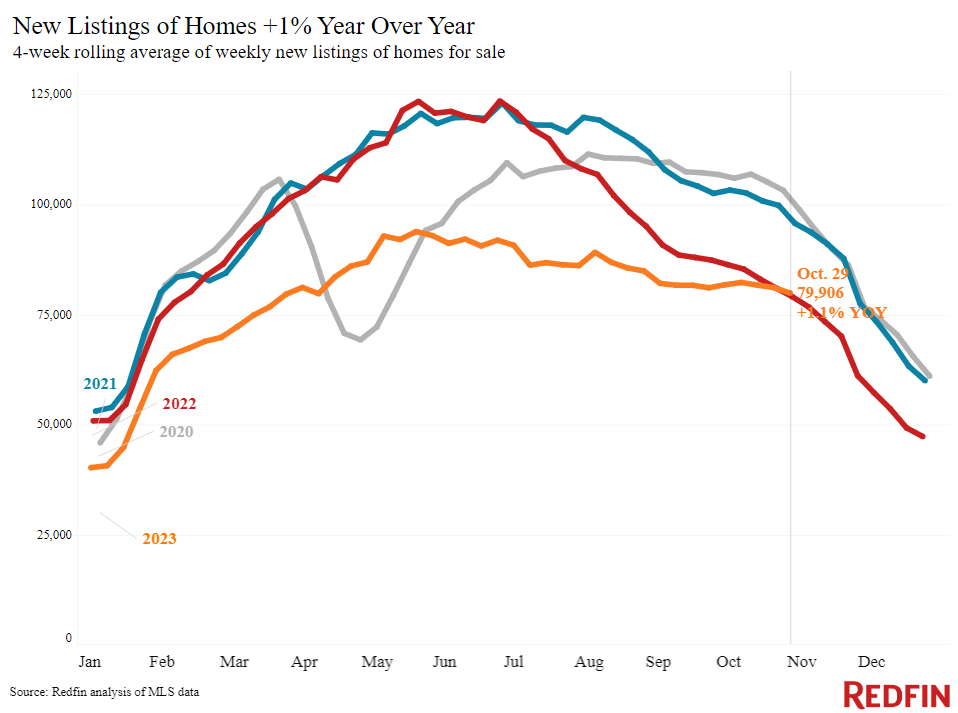

Another reason for rising sale prices is that despite slow demand, low inventory is propping up prices. The total number of homes for sale is down 10% year over year; new listings are up 1% from a year ago–just the second increase since July 2022–but that’s partly due to new listings falling quickly at this time last year. Price drops becoming more prevalent than ever while prices continue increasing illustrates today’s bizarre housing market. Redfin agents describe a mismatch between sellers’ high expectations and the reality of buyers’ budgets, saying it’s more important than ever for sellers to price fairly from the start to attract buyers and sell quickly.

“Some sellers are pricing too high because they have FOMO after their neighbor’s house sold well over asking price two years ago,” said Seattle Redfin Premier agent Patrick Beringer. “While low inventory is driving some competition and relatively affordable homes in popular neighborhoods are still selling fast, they’re getting two or three offers as opposed to 20 offers at the height of the market. With mortgage rates in the 7.5% to 8% range, buyers simply don’t have the budget they would have had two years ago or even one year ago.”

In the Seattle metro, for instance, the typical homebuyer’s monthly mortgage payment is $232 more than it would have been a year ago. It’s nearly $2,000 more than it would have been two years ago.

Refer to our metrics definition page for explanations of all the metrics used in this report.