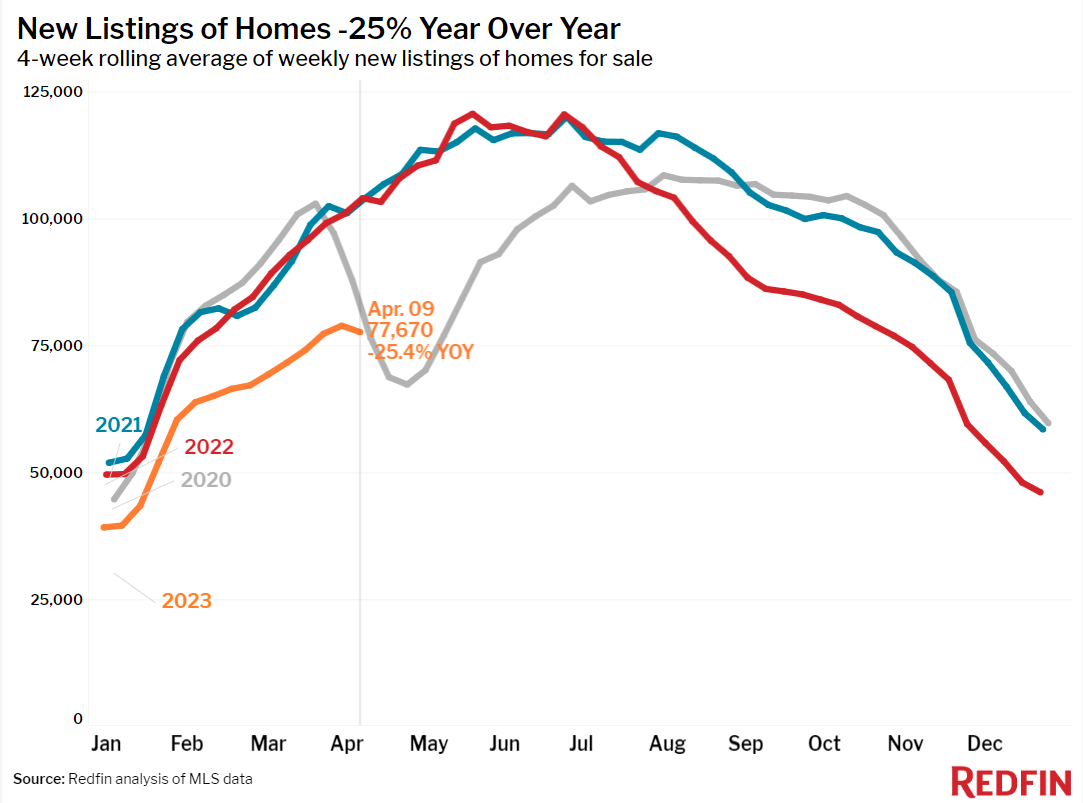

New listings of homes for sale are down 25% from a year ago, marking the eighth straight month of double-digit declines. That’s making it difficult for buyers to find homes but giving some sellers a competitive edge.

New listings of U.S. homes for sale dropped 25% from a year earlier during the four weeks ending April 9, continuing an eight-month streak of double-digit declines. That’s the biggest drop since the start of the pandemic, but there was a holiday weekend effect: Easter fell a week earlier this year than last year, so it’s likely that last weekend’s holiday made the new-listings decline larger than it would have been if Easter fell during last year’s comparison period.

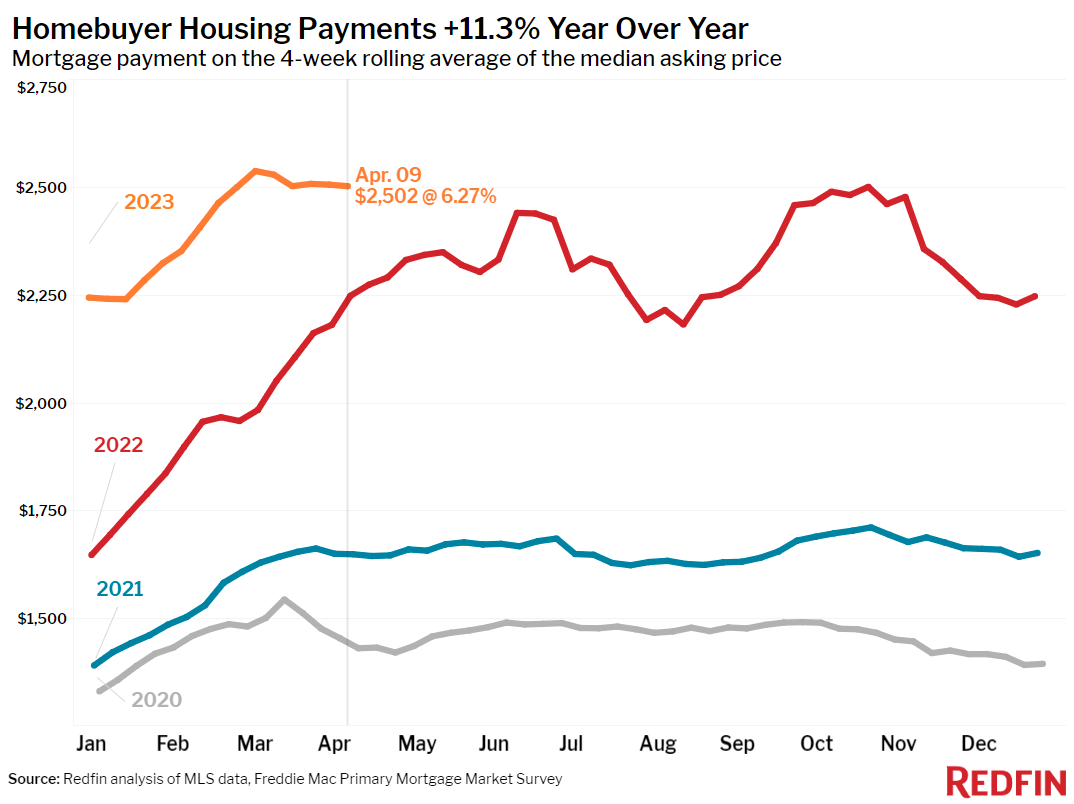

People are reluctant to sell because they don’t want to give up their low mortgage rate, it’s hard to find another home to buy and many Americans recently moved. Although rates are down from their November peak, this week’s average is 6.27%; 85% of homeowners have a rate far below 6%. The bright side for homeowners who are listing now is that desirable, well-priced homes are being snapped up in bidding wars in markets where demand outpaces supply.

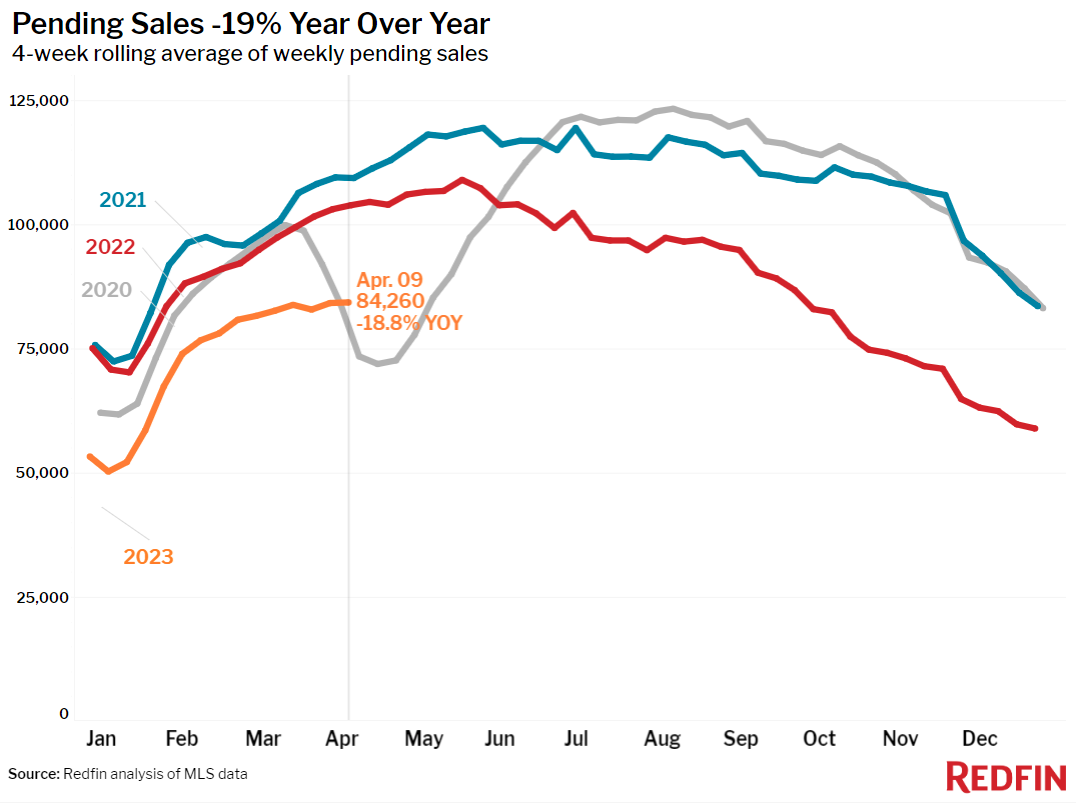

New listings fell from a year earlier in all 50 of the most populous U.S. metros, with the biggest declines in California. They dropped most in Sacramento and Oakland (-47% YoY apiece), San Francisco (-43.2%), San Jose (-42.9%) and San Diego (-41.4%). The scarcity of homes hitting the market, along with elevated mortgage rates, is holding back sales. Pending home sales dropped more than 30% in each of those metros, more than the 19% nationwide decline.

While pending sales are down, early-stage homebuying demand is ticking up, with mortgage-purchase applications up 8% from a week earlier, seasonally adjusted.

Angela Langone, a Redfin agent in San Jose, said there aren’t enough listings to go around, with multiple offers on many homes. Both new listings and pending sales are down more than 40% from a year ago in San Jose.

“Many buyers here aren’t held back by high mortgage rates; it’s the lack of inventory that’s really getting in their way,” Langone said. “I have several clients who are serious about buying a home and they’re actively looking, but they can’t find anything right now and they’re waiting for more homes to trickle onto the market.”

Buyers have more options in other parts of the country. In Nashville, TN, for instance, new listings and pending sales were both down about 14% from a year earlier–but those are some of the smallest drops in the country.

“Inventory isn’t a major problem here because the greater Nashville area is so sprawling, and there are a lot of newly built homes on the market in the suburbs,” said Nashville Redfin agent Jennifer Bowers. “Builders went big in the outskirts of the city over the last few years and now they’re offering incentives to attract buyers, to the point where individual sellers are having a hard time competing. For buyers willing to stray from the city center, there are plenty of homes for sale.”

Two new pieces of economic data serve as tea leaves we can read to anticipate how mortgage rates will trend over the next few months: It’s unlikely they’ll skyrocket, but it’s also unlikely they’ll come down enough to motivate locked-in homeowners to sell. The March consumer-price index and jobs report showed that inflation continued to cool and wage growth ticked down from the month before, but inflation is still higher than the Fed’s target.

“The Fed has made some progress cooling inflation with rate hikes but there’s still work to be done,” said Redfin Chief Economist Daryl Fairweather. “Even if the Fed chooses not to hike rates next month, which would likely bring down mortgage rates, the limited supply of homes for sale would remain a major obstacle for would-be buyers. Rates dipping below 6% would probably pique the interest of more buyers, but enough homeowners have rates in the 3% or 4% range that we’re unlikely to see a big uptick in new listings.”

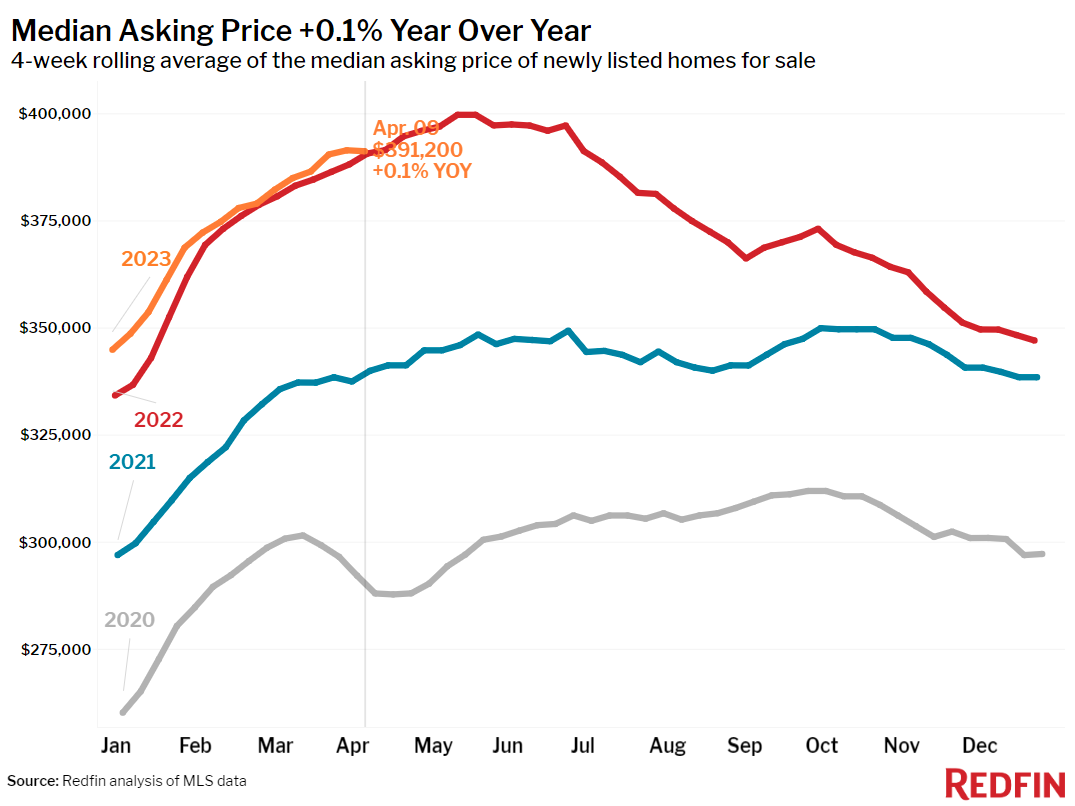

The median U.S. home-sale price fell 2.3% year over year to roughly $364,000, the biggest decline in more than a decade.

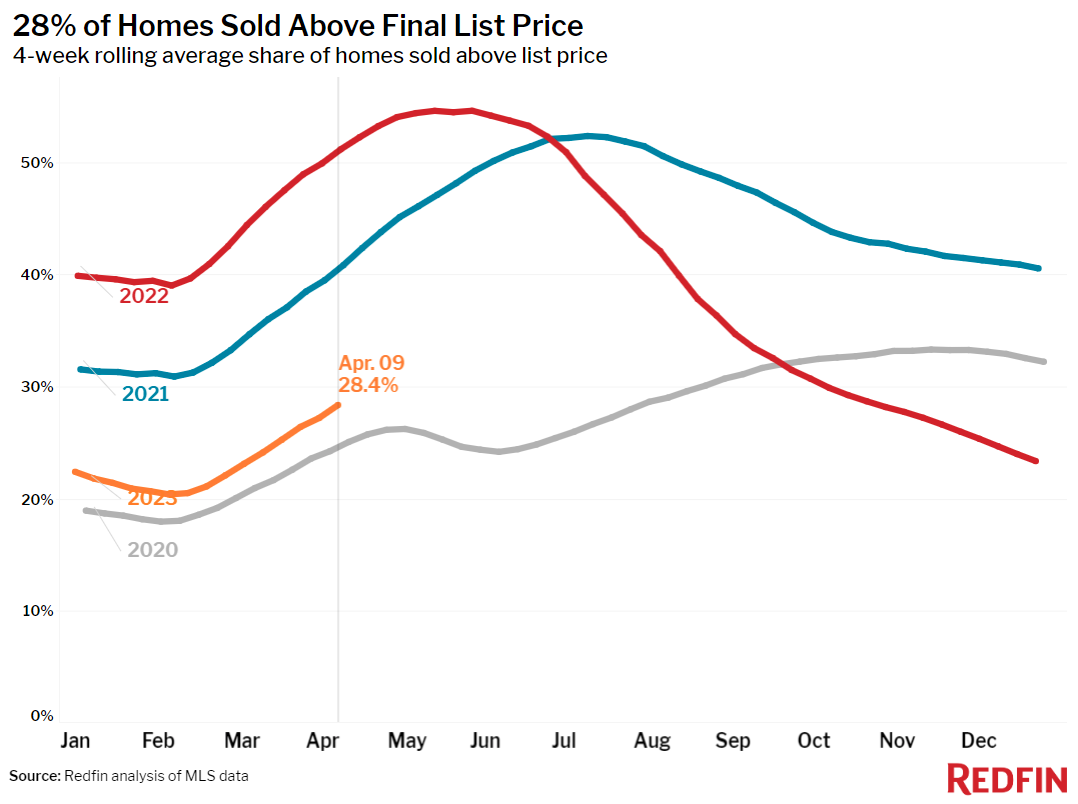

Prices fell significantly more than that in some metros, but rose in others. Home-sale prices dropped in more than half (29) of the 50 most populous U.S. metros, with the biggest drop in Austin, TX (-13.9% YoY). Next come four West Coast metros: Oakland (-11.4%), San Francisco (-10.9%), Seattle (-10.9%) and Sacramento (-10.6%). That’s the biggest annual decline since at least 2015 for Seattle.

On the other end of the spectrum, sale prices increased most in Fort Lauderdale, FL, where they rose 11.6% year over year. Next come Milwaukee (9.5%), Miami (8.5%), Cincinnati (7.3%) and Providence, RI (7.2%).

Unless otherwise noted, the data in this report covers the four-week period ending April 9. Redfin’s weekly housing market data goes back through 2015.

Refer to our metrics definition page for explanations of all the metrics used in this report.