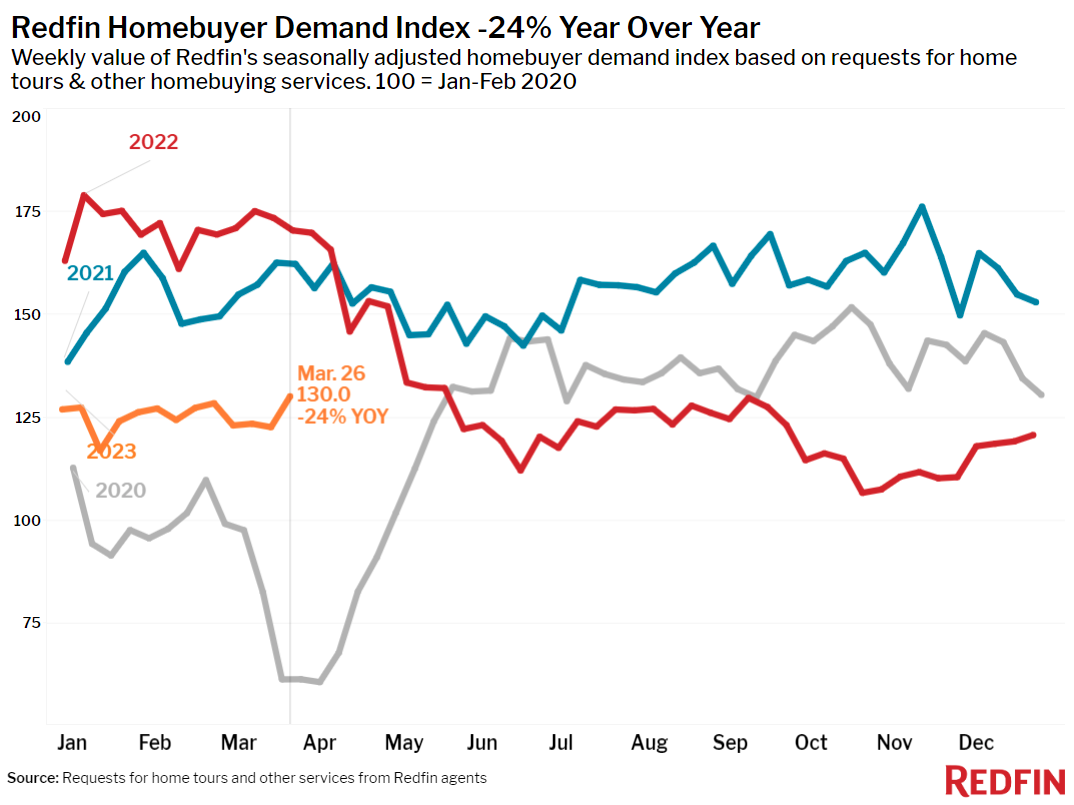

Redfin’s Homebuyer Demand Index, which measures requests for tours and other buying services from our agents, jumped as prices fell for the sixth-straight week and mortgage rates declined for the third week in a row. But a lack of new listings is holding back sales.

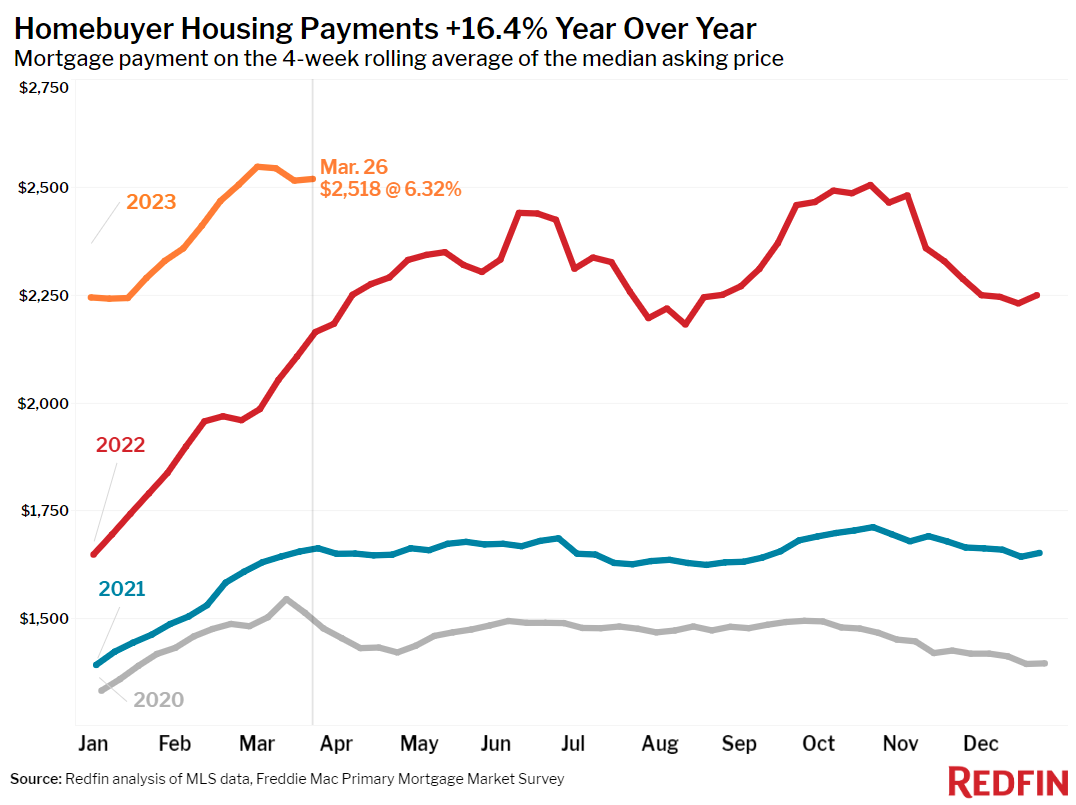

House hunters are wading into the market as mortgage rates and home prices continue to decline. Mortgage-purchase applications increased for the fourth week in a row and Redfin’s Homebuyer Demand Index–a seasonally adjusted measure of requests to tour homes, make an offer on a home and/or start a home search with a Redfin agent–jumped to its highest level since last May during the week ending March 26.

“My phone is ringing, and it’s usually first-time buyers or investors,” said San Francisco Redfin agent Ali Mafi. “First-time buyers are interested in looking at homes because prices have come down, though they’re still concerned about high mortgage rates. Investors who can pay in cash are honing in on luxury San Francisco condos because prices on those have dropped even more significantly than the overall market.”

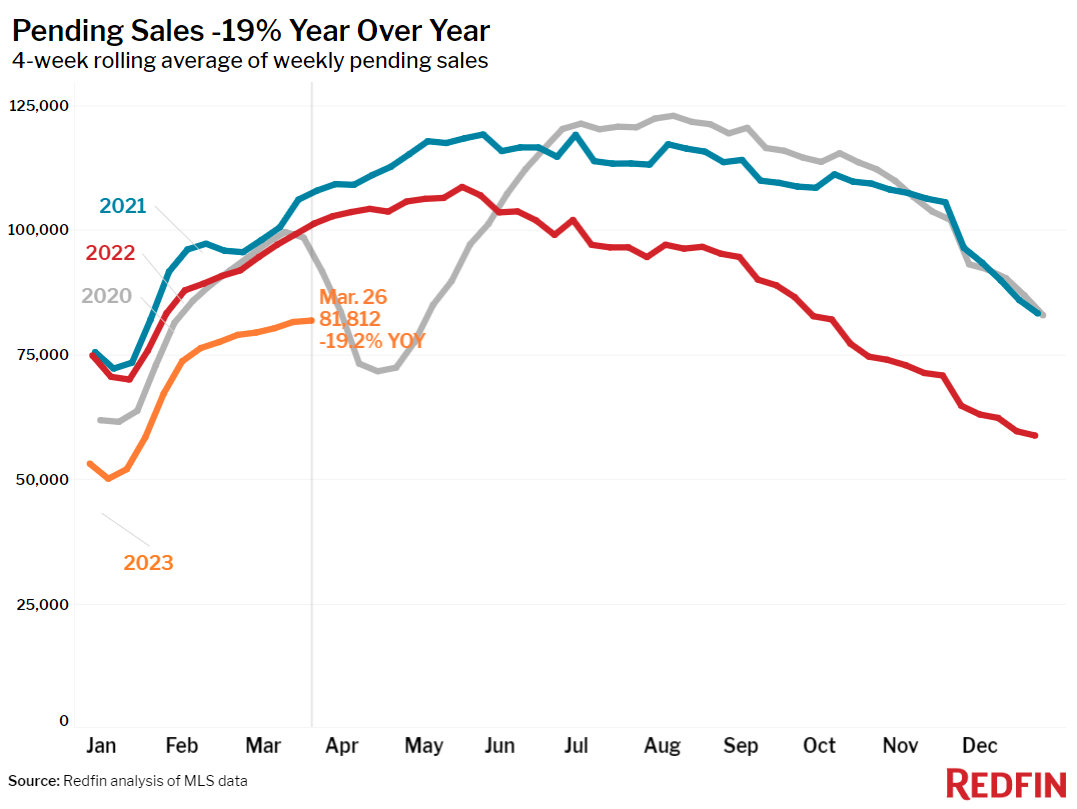

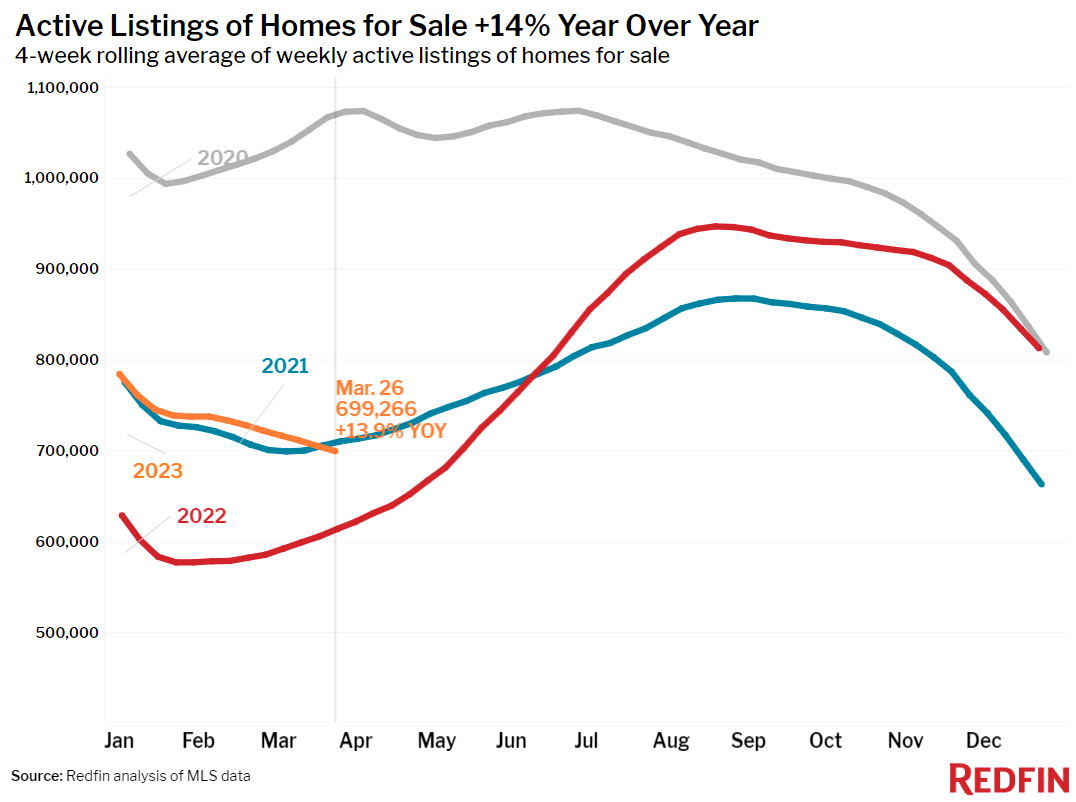

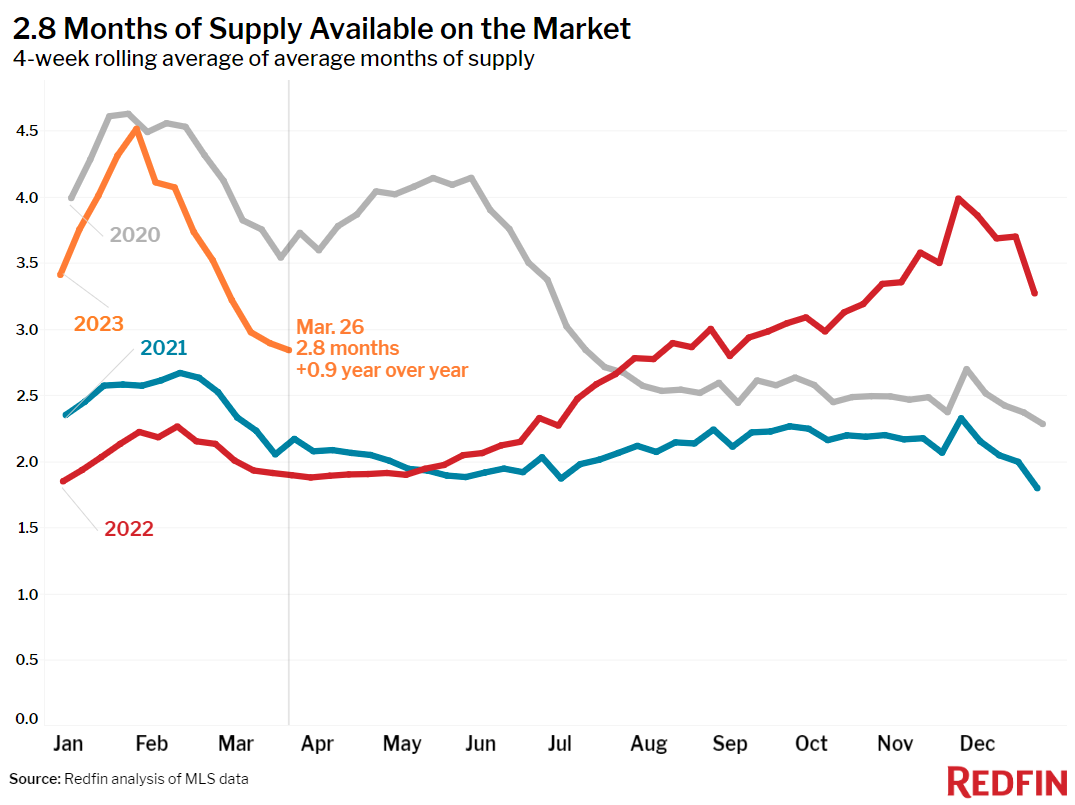

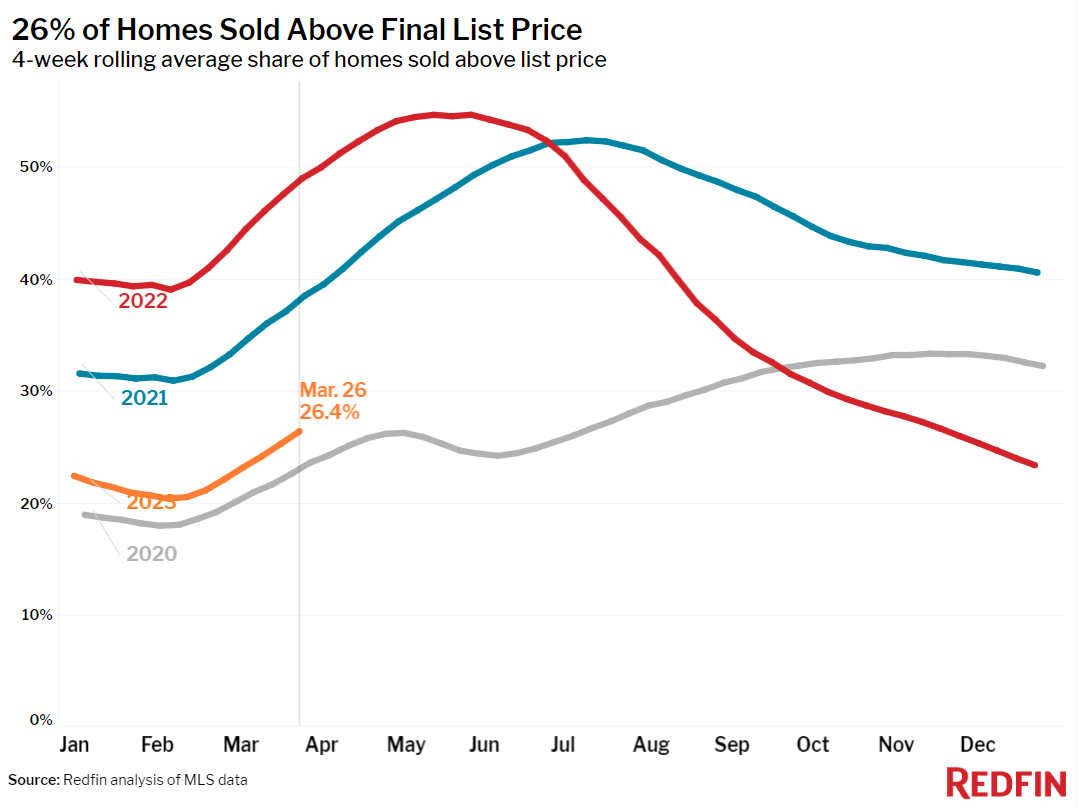

The uptick in early-stage demand has yet to translate into more home sales. Pending sales dropped 19% year over year nationwide in the four weeks ending March 26, the biggest decline in about two months. Demand for homes hasn’t yet translated into an improvement in sales mainly because would-be buyers are limited by lack of supply.

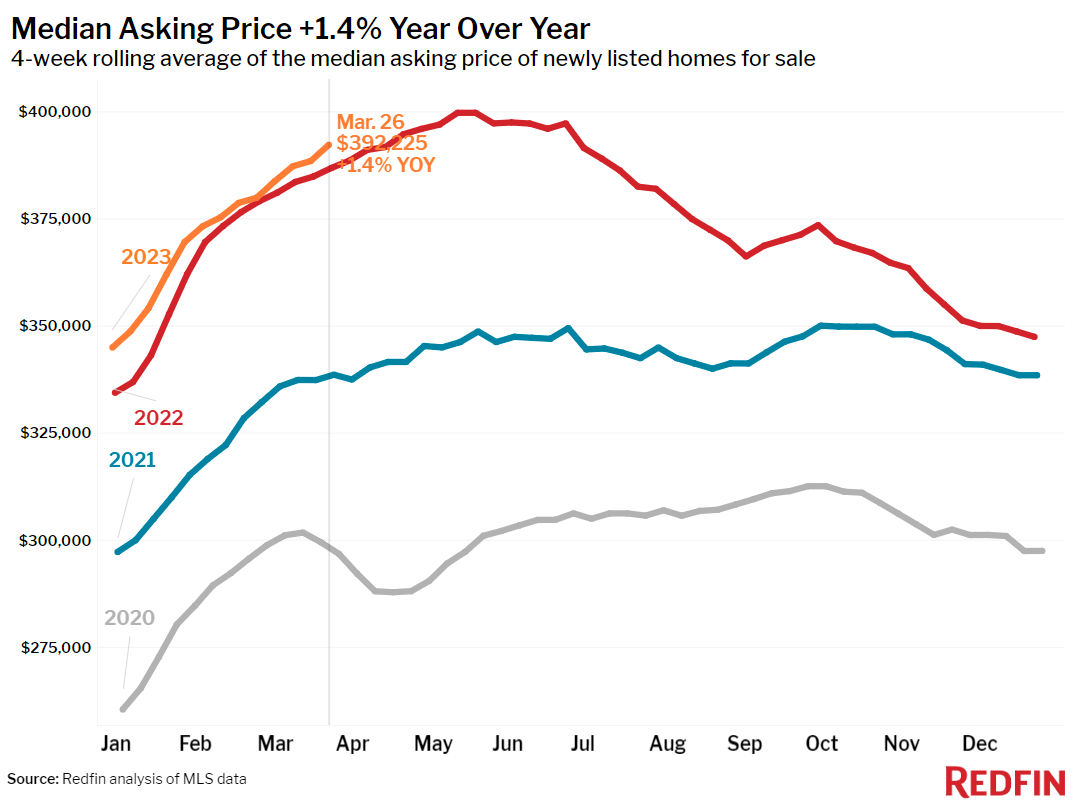

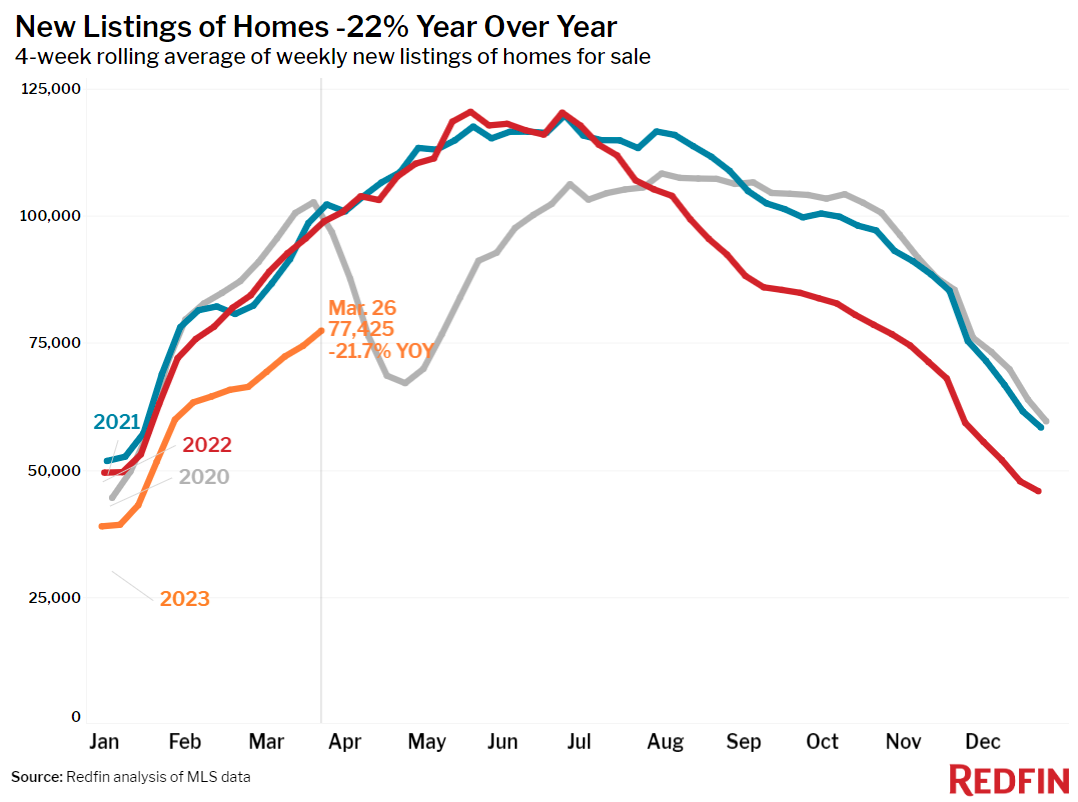

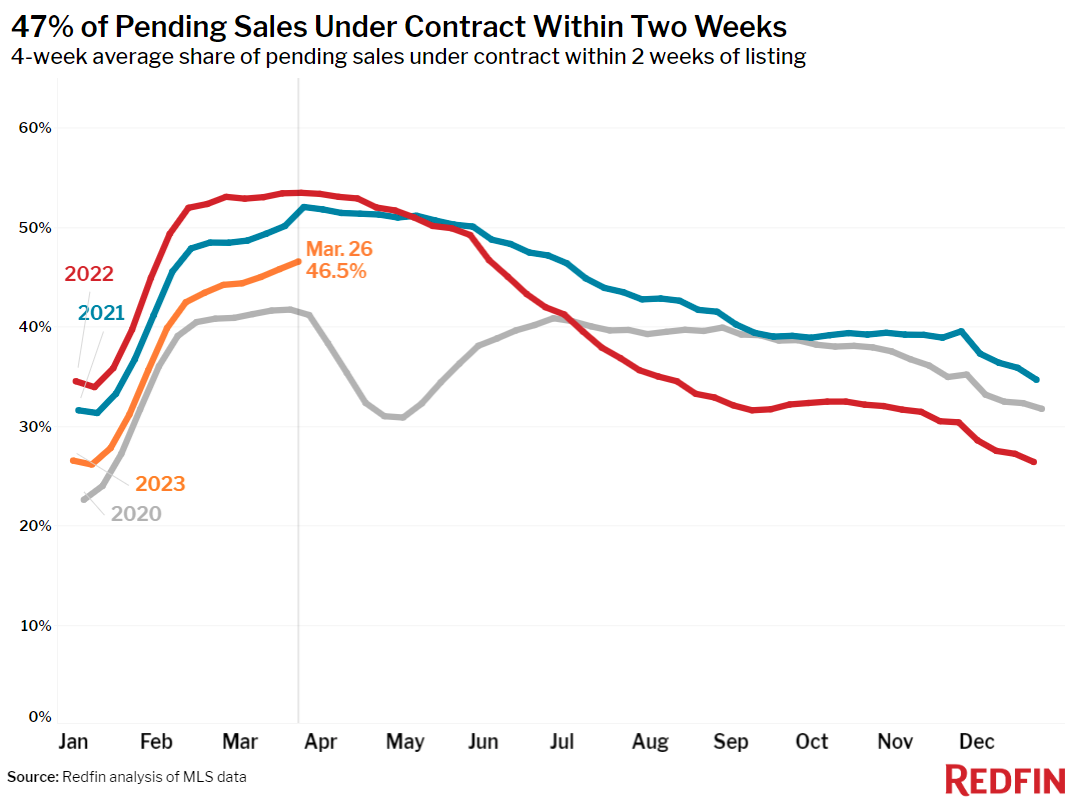

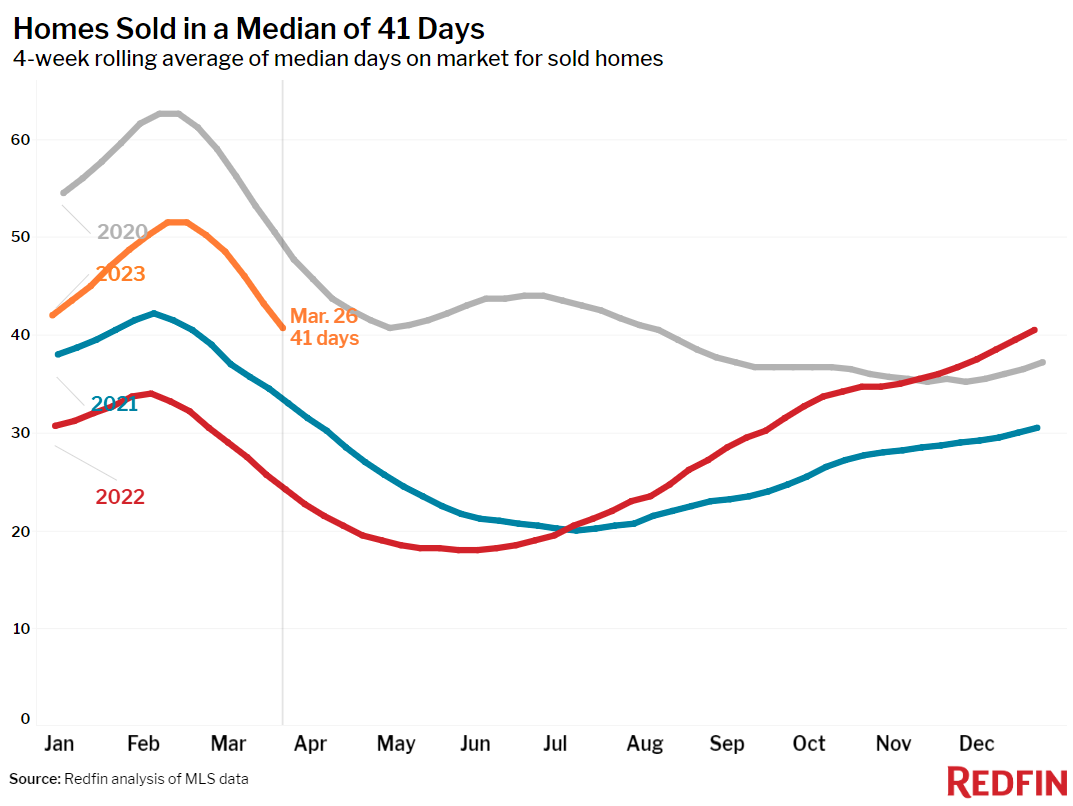

New listings of homes for sale declined 22%, one of the biggest drops since the start of the pandemic; homeowners are reluctant to sell because they don’t want to give up a low mortgage rate. The lack of new listings is causing a growing share of homes to fly off the market quickly: Nearly half of homes are selling within two weeks, the largest share since June.

While the scarcity of new listings is holding back sales nearly everywhere in the U.S., prices are dropping fast in some parts of the country and increasing in others.

Home prices dropped in more than half (28) of the 50 most populous U.S. metros, with the biggest drop in Austin, TX (-15.2% YoY). Next come four northern California metros: San Jose, CA (-12.9%), San Francisco (-11.7%), Sacramento, CA (-11.4%), and Oakland, CA (-10.8%). Those are the biggest annual declines since at least 2015 for Austin and Sacramento.

On the flip side, sale prices increased most in Milwaukee, where they rose 14.1% year over year. Next come Fort Lauderdale, FL (8.5% YoY), Virginia Beach, VA (6.9%), West Palm Beach, FL (6.7%) and Providence, RI (6.4%).

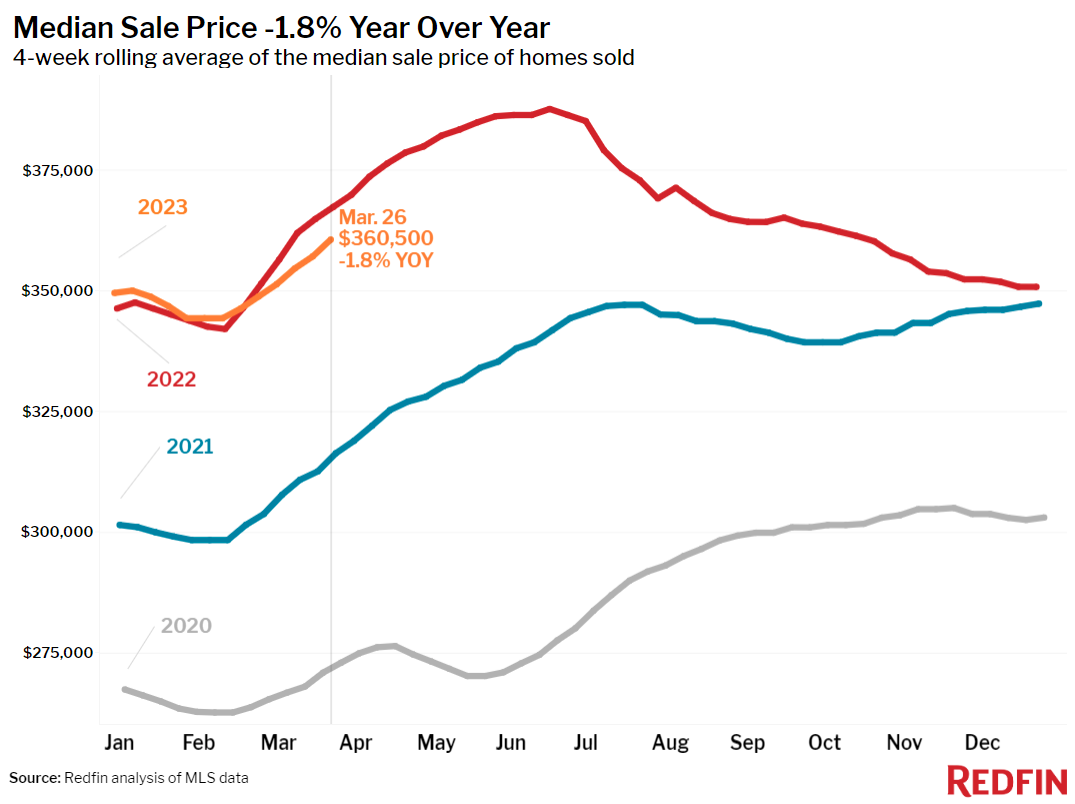

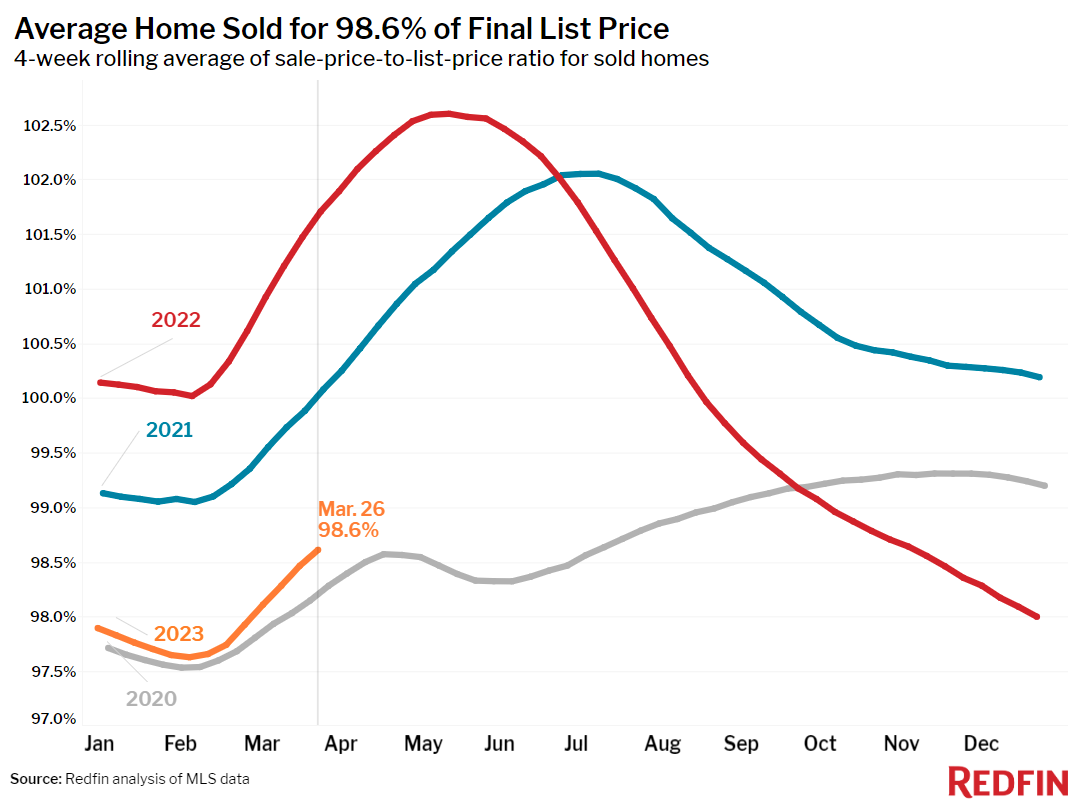

On a national level, the median U.S. home-sale price fell 1.8% year over year to $360,500, marking the sixth straight week of declines after more than a decade of increases.

“Prices are still rising quickly in some places while they are down by double digits in big tech hubs, so it’s important for prospective buyers to work with an expert local agent,” said Redfin Deputy Chief Economist Taylor Marr. “One thing that’s true almost everywhere: It’s difficult to find a desirable, well-priced home for sale, so offer and negotiation strategies differ depending on where you’re looking.”

Unless otherwise noted, the data in this report covers the four-week period ending March 26. Redfin’s weekly housing market data goes back through 2015.

Refer to our metrics definition page for explanations of all the metrics used in this report.