More sellers are listing their homes, but 7% mortgage rates and still-high home prices are pushing down sales.

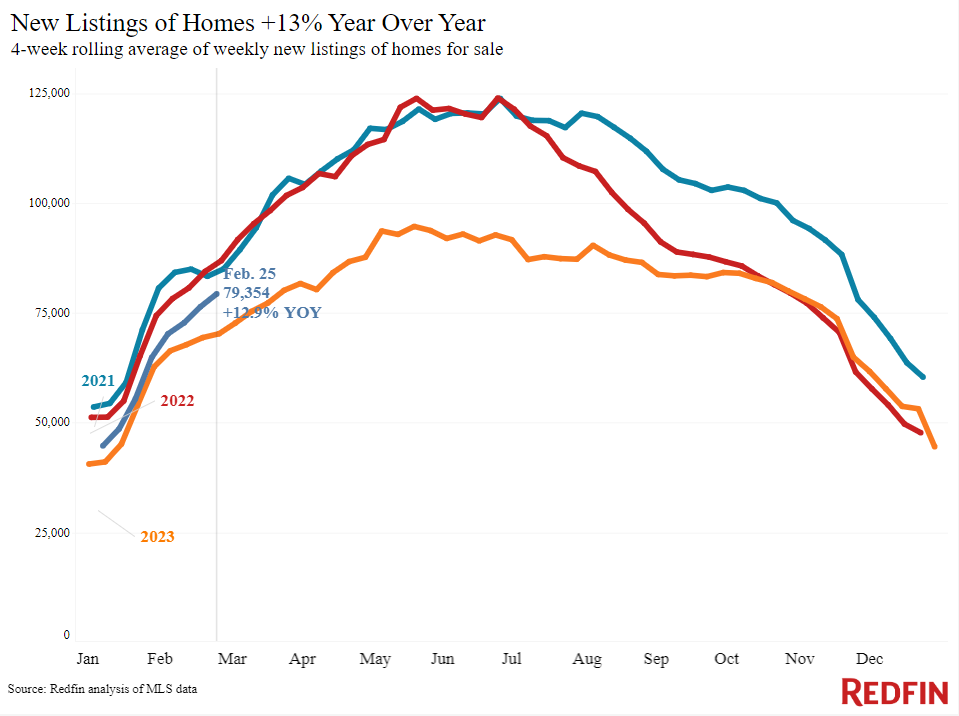

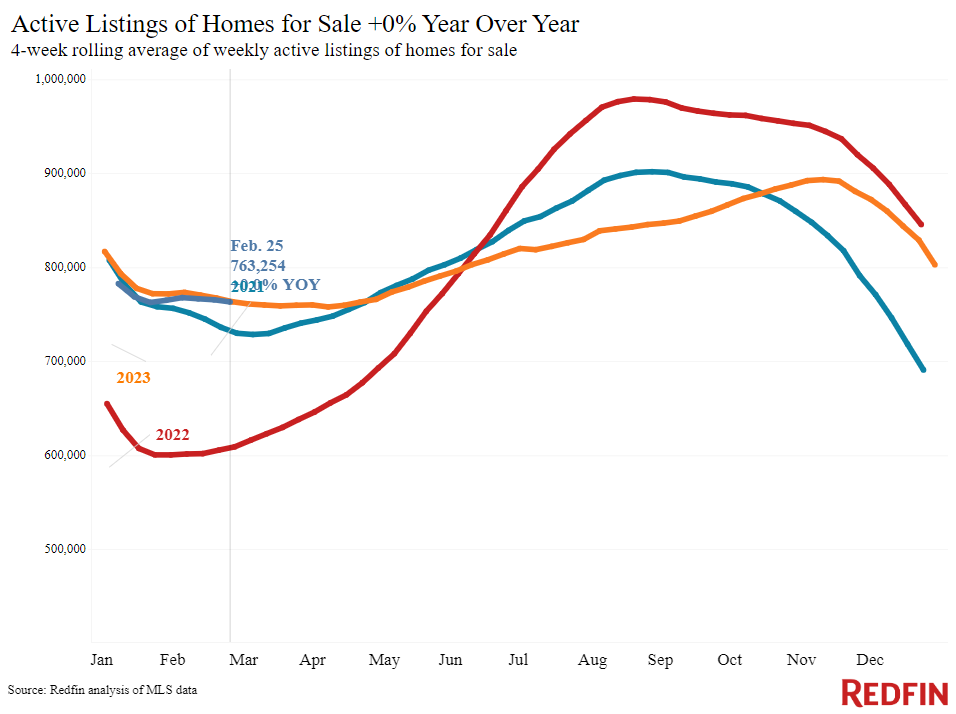

New listings of U.S. homes for sale rose 13% year over year during the four weeks ending February 25, the biggest increase in nearly three years. Total inventory is also improving: Active listings are flat from a year ago, marking the first time in nine months the total number of homes for sale hasn’t declined.

That’s welcome news for homebuyers, who have been battling the dual challenges of low inventory and high mortgage rates for over a year. But while today’s buyers have a few more homes to choose from, they’re still facing historically high housing costs. The typical homebuyer’s mortgage payment is $2,671, just $47 shy of last October’s record high.

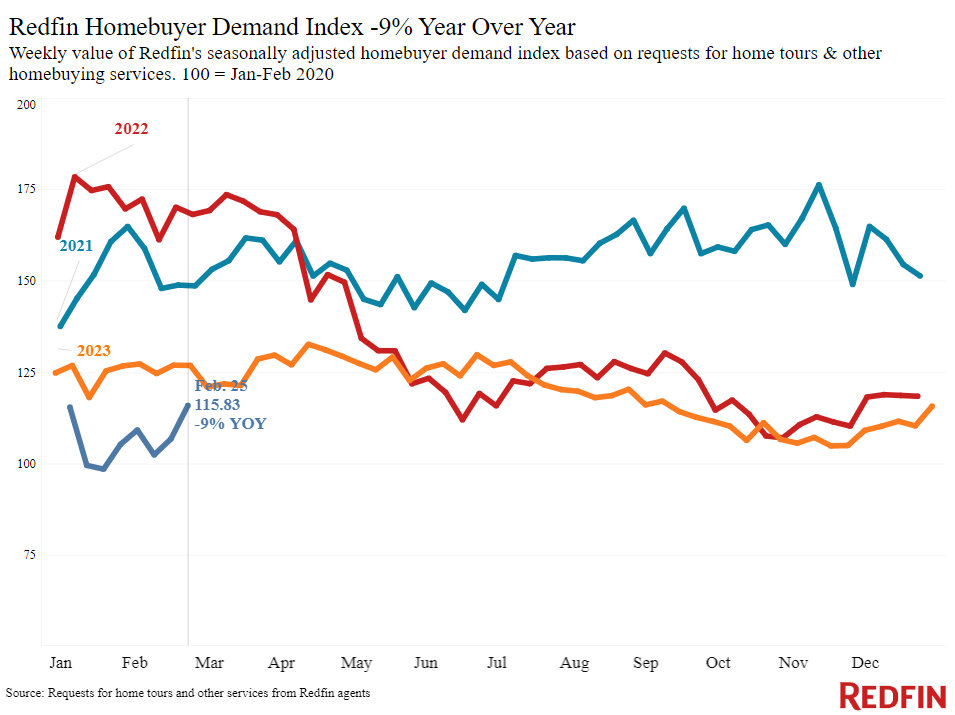

High costs pushed pending sales down 8%, the biggest decline in five months, and mortgage-purchase applications declined for the fourth straight week. But more house hunters are out there searching as more homes hit the market. Redfin’s Homebuyer Demand Index–a measure of requests for tours and other services from Redfin agents–is up 10% from a month ago to its highest level since last September. Pending sales could improve in the next few months if rates don’t increase further and new listings continue to rise.

“House hunters are out there, and competition picks up every time mortgage rates decline a bit,” said Brynn Rea, a Redfin Premier agent in Spokane, WA. “I’m telling buyers who can afford it to look now while they have more breathing room and less competition. They have a good chance of negotiating the price down or getting some concessions from the seller, which could make up for getting a 7% mortgage rate instead of 6%.”

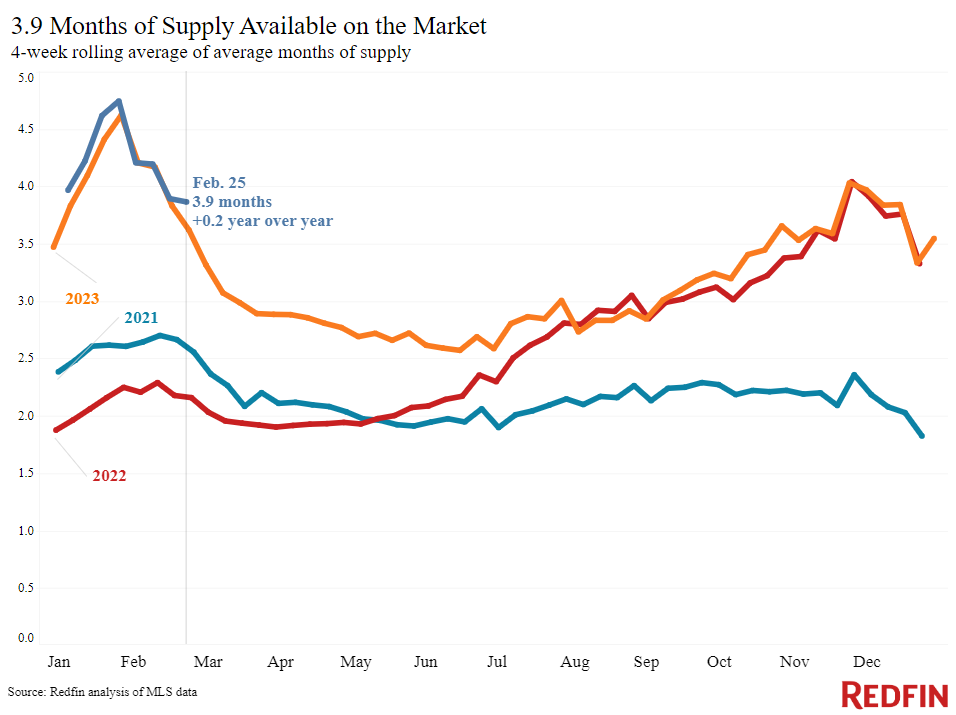

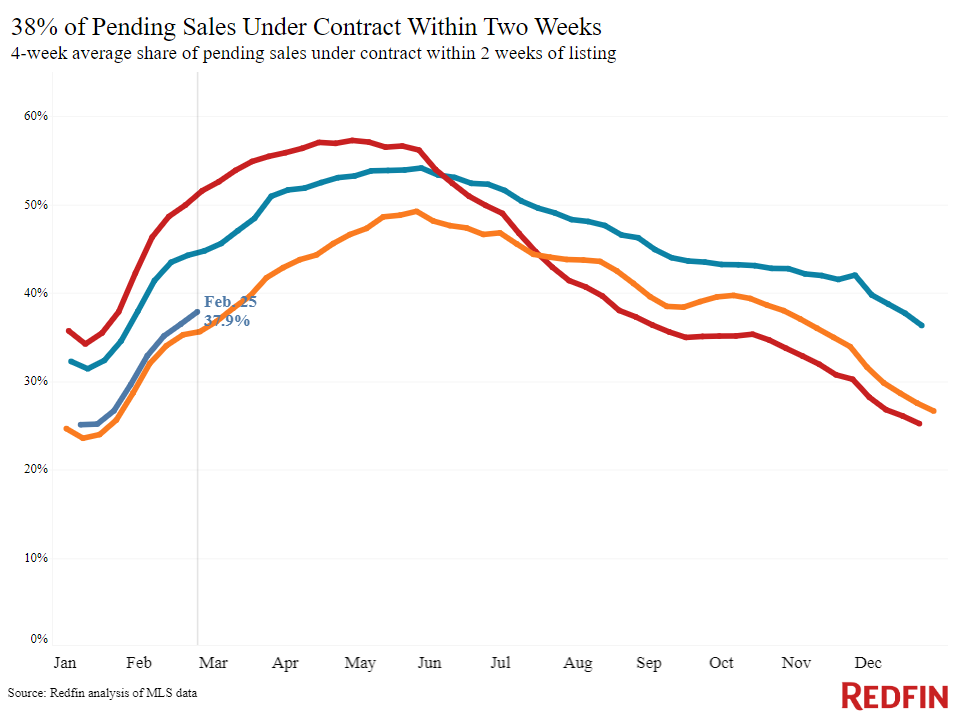

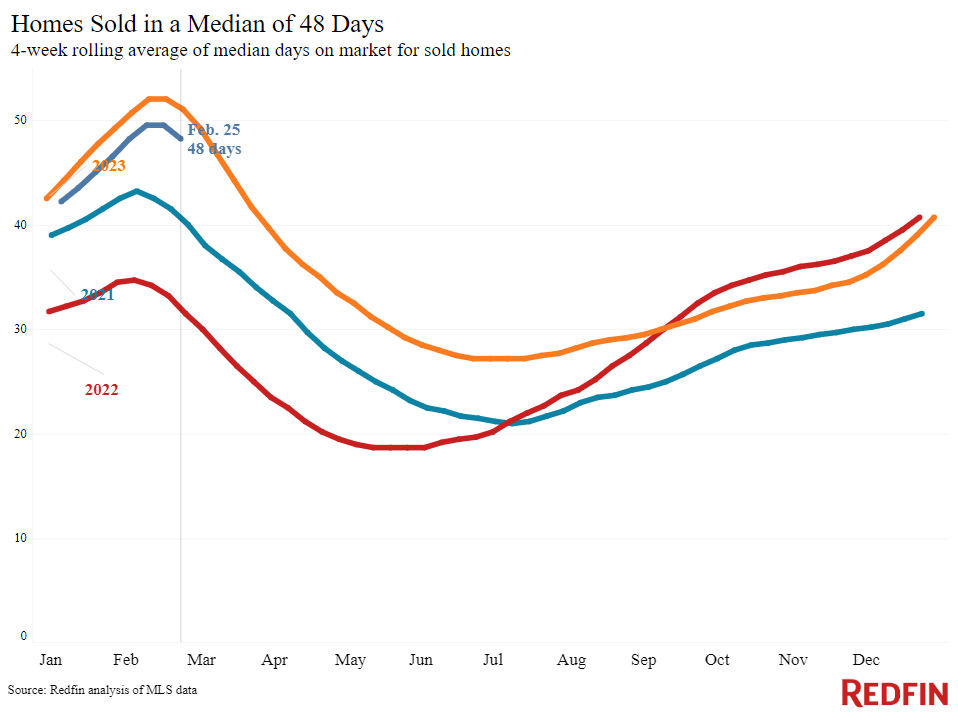

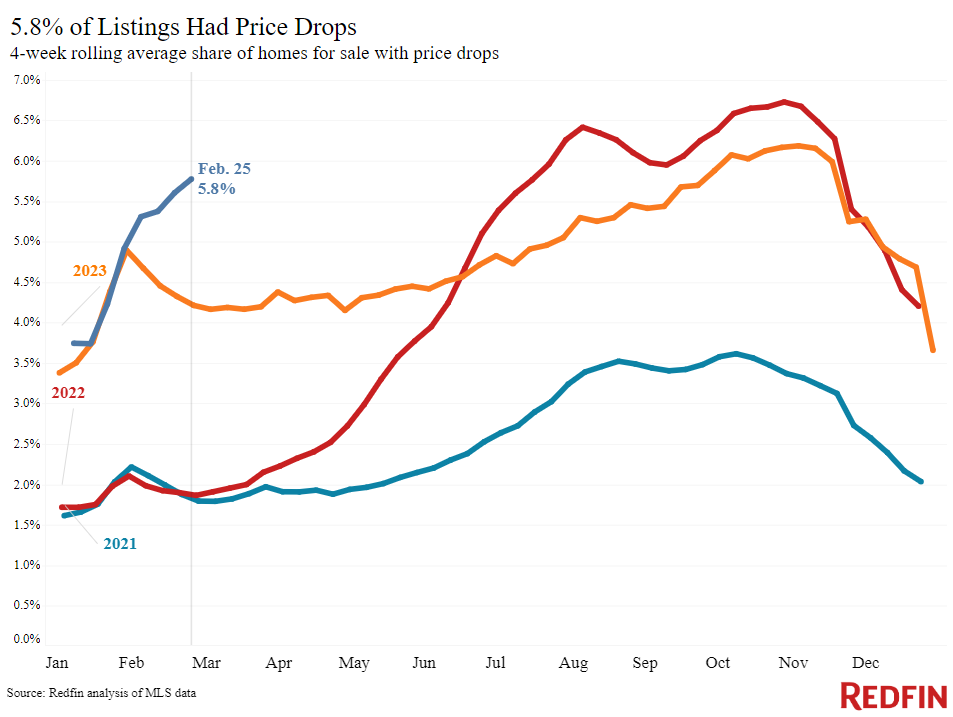

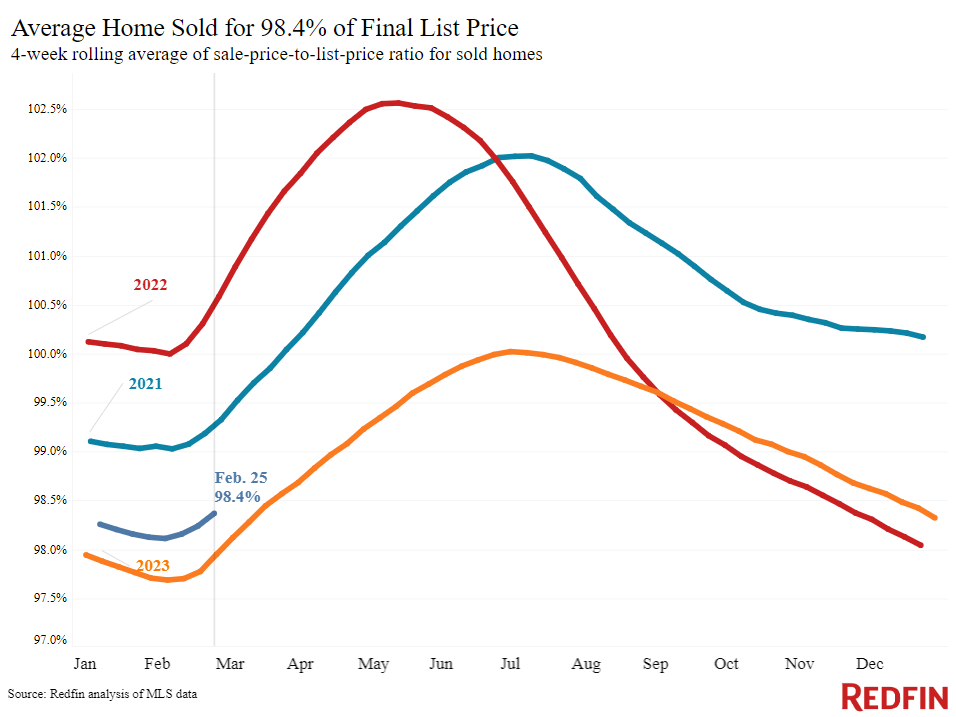

Refer to our metrics definition page for explanations of all the metrics used in this report.