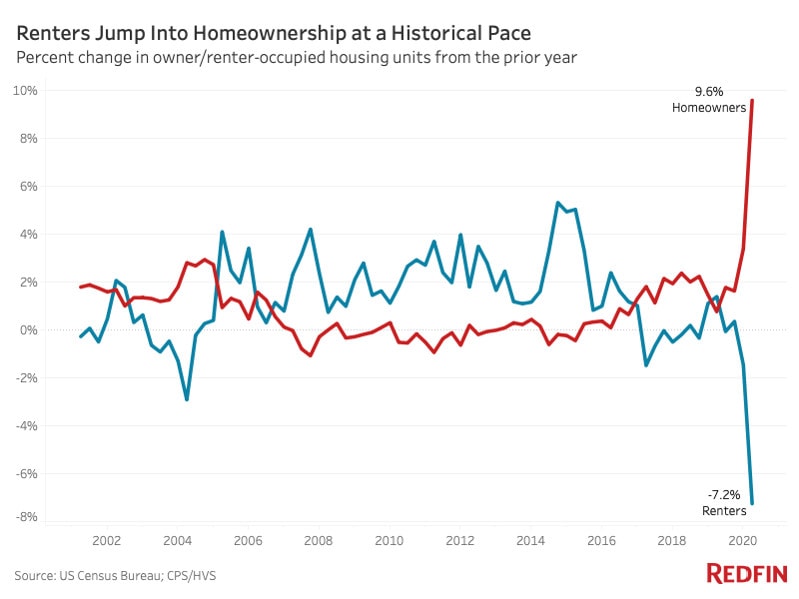

Homeownership rates surged to 67.9% in the second quarter, the highest rate since 2008. The 3.8 percentage point increase from 64.1% a year earlier is the largest annual increase in homeownership rates on record. A word of caution about the data: The Census changed its methodology this quarter, eliminating all in person interviews due to the pandemic, which may have distorted the data and contributed to such a large jump in homeownership rates. That said, there are a number of intertwined pandemic-related trends that have likely led to the strong growth in homeownership:

The homeownership rate climbed the most among 35-44 year olds (up 4.9 percentage points to 64.3%) and people under 35 (up 4.2 percentage points to 40.6%). Demographically, we anticipated the homeownership rate would grow in 2020 and beyond because a huge wave of millennials are entering their prime homebuying years. The pandemic may have moved up this timeline in the short-run. Many renters who had perhaps been planning a purchase in the next few years, have opted to go ahead and buy now given historically low rates. Thus the current growth will likely not continue to climb as much in future quarters. These low rates hit at a time when apartment living is at its least desirable. People confined to their homes aren’t able to take advantage of communal building amenities or the neighborhood retail and restaurants that make renting in an urban area appealing.

As we spend more time at home, home is more important than ever and Redfin agents report that buyers are rethinking their priorities.

“Spending so much time at home during quarantine has made a lot of people realize that it might be time to stop renting a cramped apartment in the city and time to start owning their first single-family home,” said Pam Henderson, a Redfin agent in Dallas. “With mortgage rates at record lows and remote work on the rise, some renters are having an epiphany: They could buy a lower-priced home in the suburbs for close to what they’re paying in rent.”

Many people expect to continue working remotely at least some of the time even after the pandemic ends. As a result, buyers who were tied to renting in an expensive area near their workplace, now have the flexibility to buy a home in a more affordable suburb or even in another city entirely. Redfin’s migration data found that a record 27.4% of Redfin.com users looked to move to another metro area in the second quarter of 2020. That’s up from 25.2% in the second quarter of 2019.

Additionally, the math has shifted in the favor of buying. A half-point drop in mortgage rates can decrease a homebuyers’ monthly payment substantially, making a mortgage more attractive than a lease. Meanwhile, rents are sticky in the short term. Because renters are locked into a lease, rents don’t fluctuate like a stock price and adjust more gradually.

This is a short-term shift. In the long run, as renters opt to buy there is less demand for rental units, which will pull rents down. At the same time, the increased demand for real estate will push up home prices. So we’ll see the rent vs. buy equation rebalance over time.

The number of rental households fell by 7.2% in the second quarter. During the first wave of the pandemic, many people moved out of rental units into owner-occupied homes–often with parents or other family– either due to job loss or to leave densely populated areas like New York City during the height of the stay-at-home orders. While these moves have not created new homeowners per se, this phenomenon does contribute to the homeownership rate increasing because someone previously living in a rental unit is now counted as living in an owner-occupied unit. However, this effect was outweighed by strong growth in new household formation, which rose by 4% in June—the highest annual growth rate since the record began in 1955.