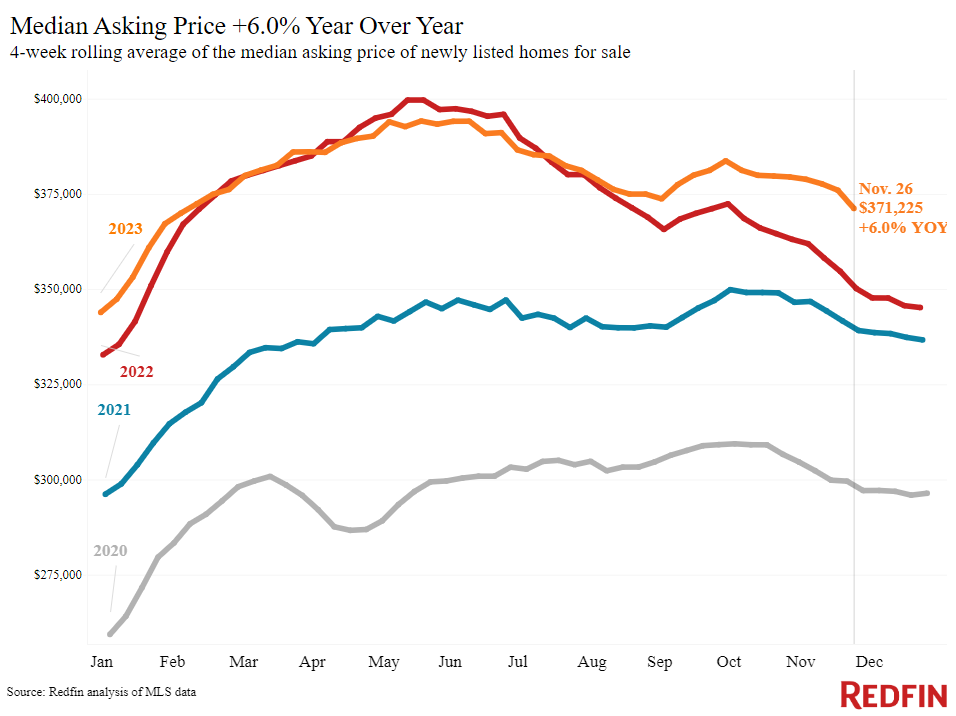

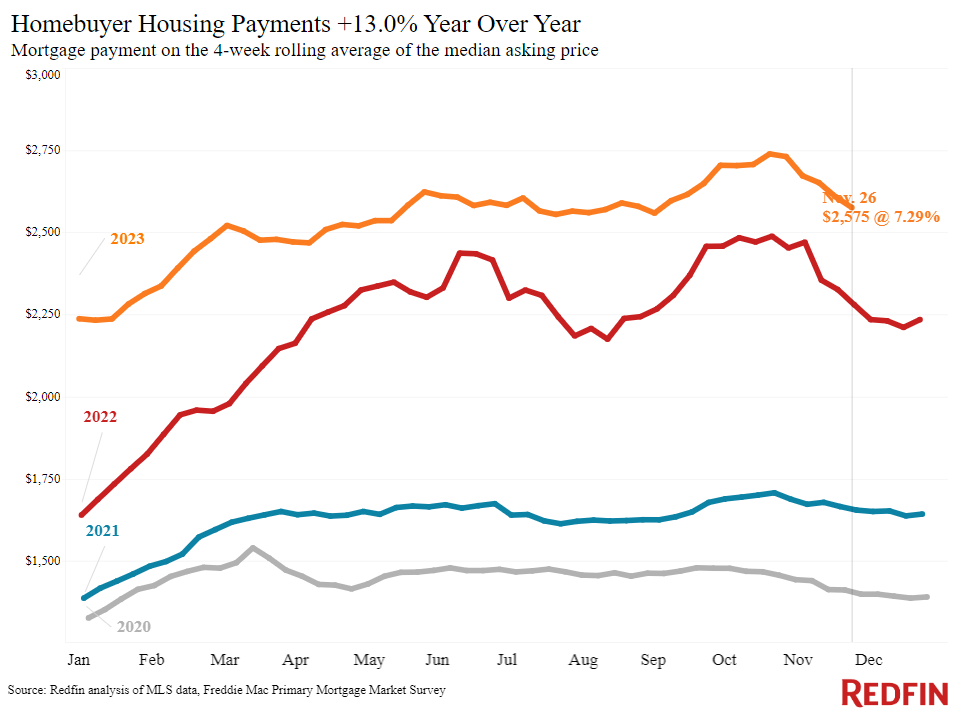

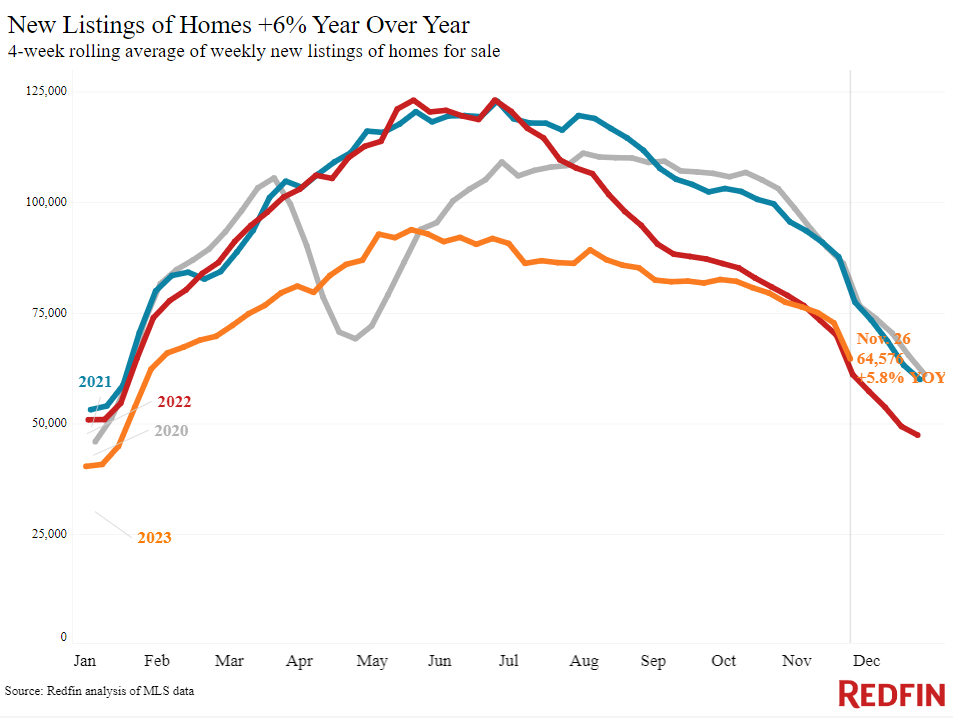

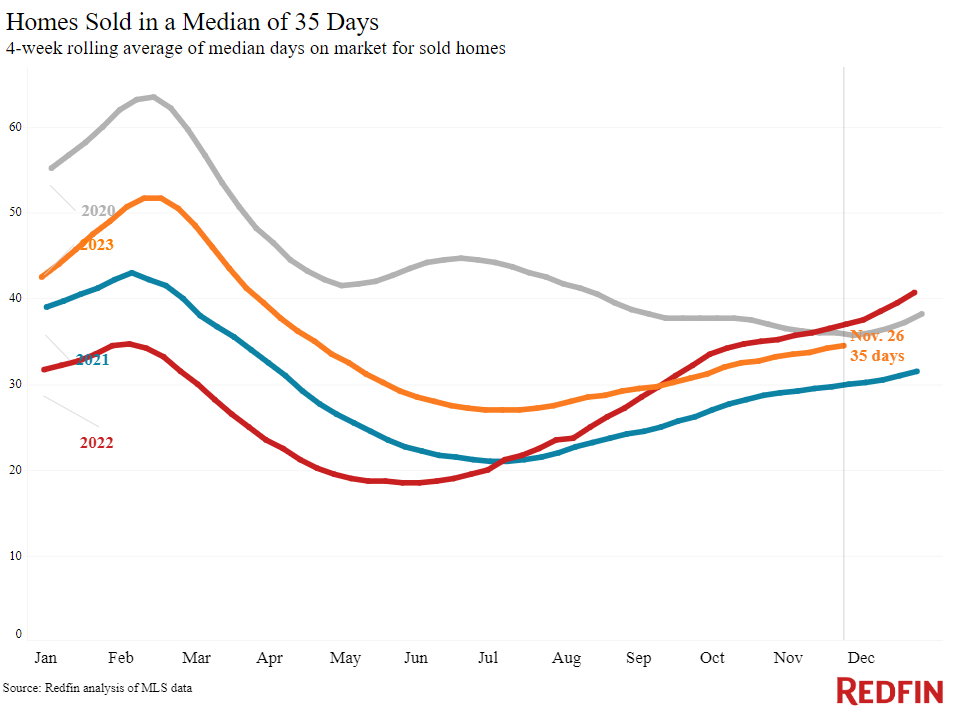

The median monthly mortgage payment has declined more than $150 from its peak to its lowest level since August. Another piece of good news for buyers: New listings are seeing their biggest year-over-year increase since summer 2021.

Housing payments have declined for the fifth week in a row. The typical U.S. homebuyer’s monthly mortgage payment was $2,575 during the four weeks ending November 26, down $164 from a peak of $2,739 last month but up 13% year over year.

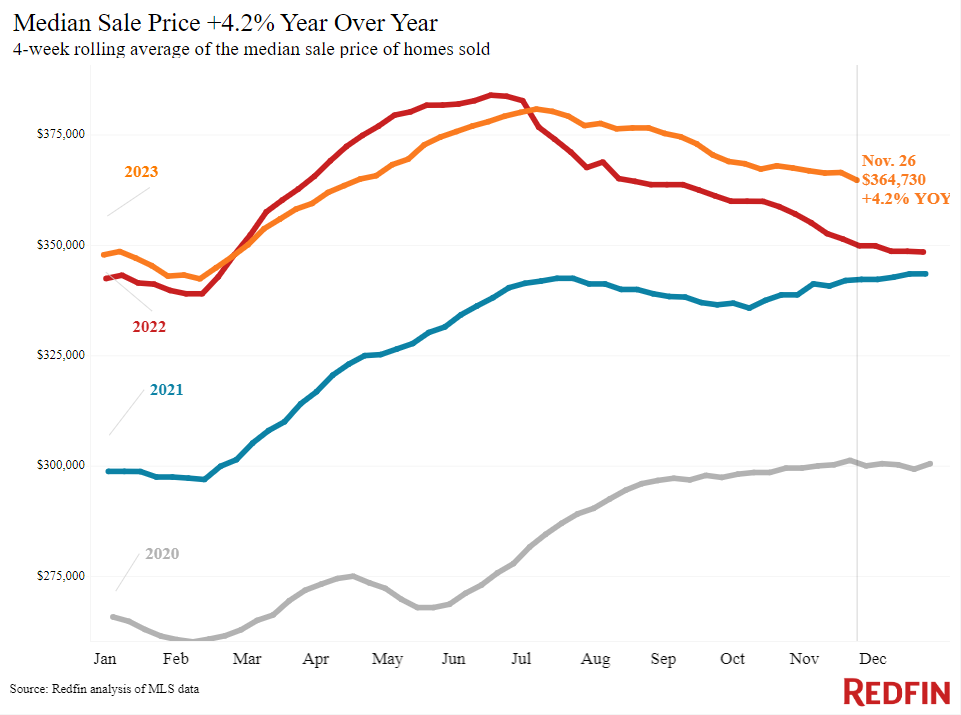

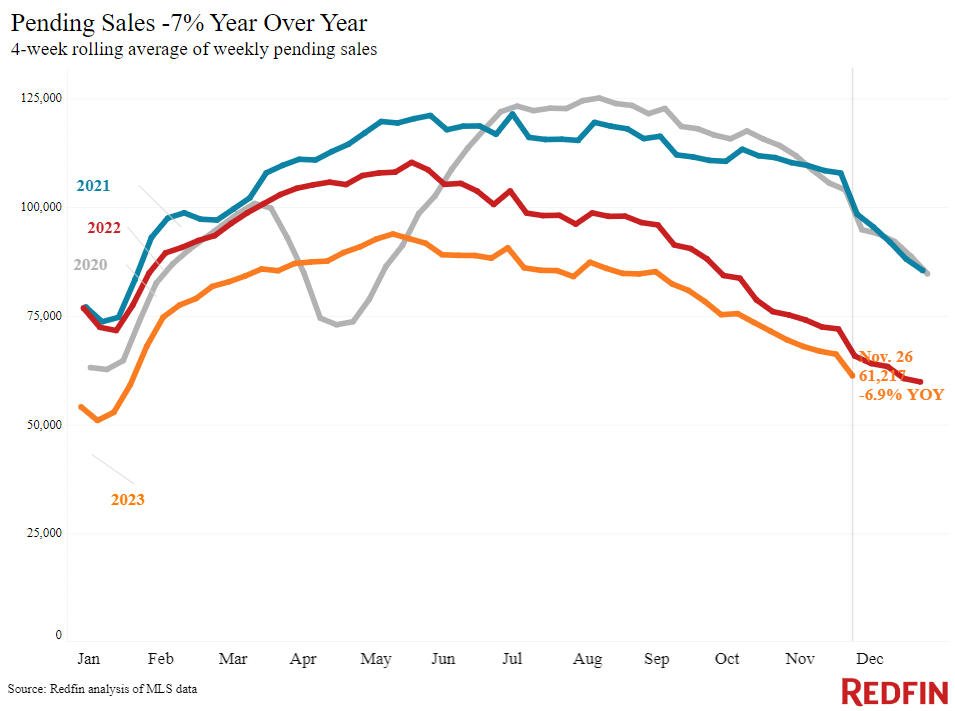

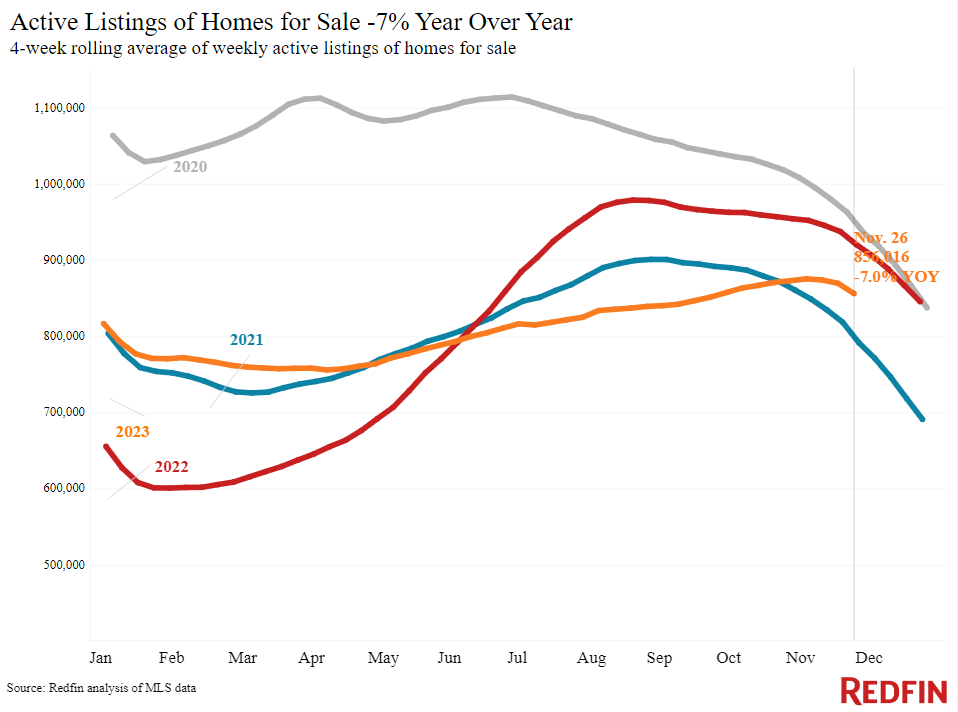

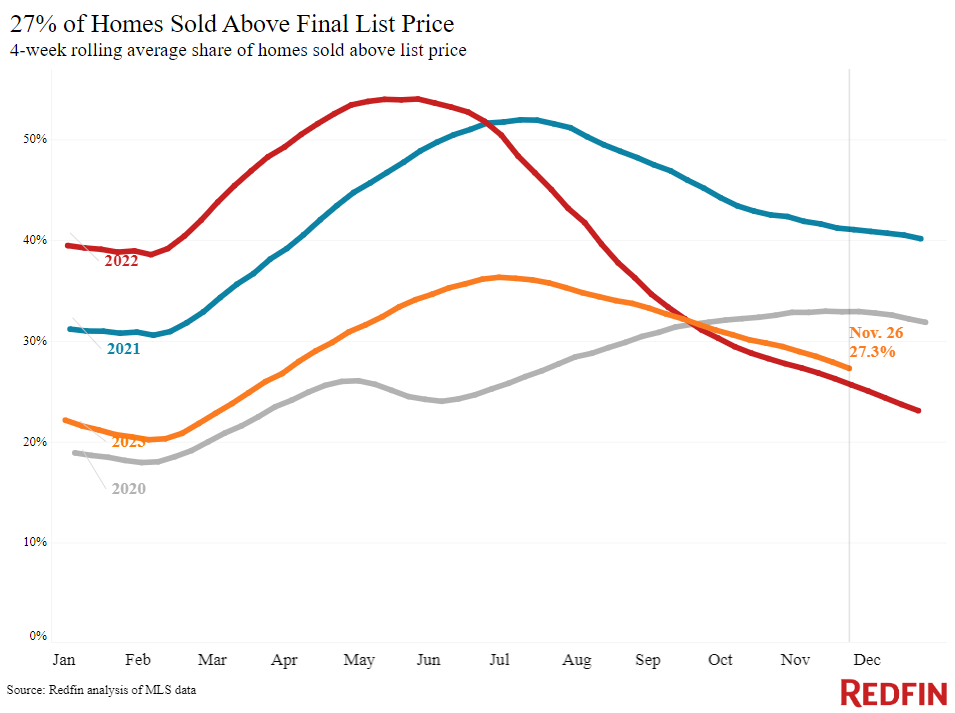

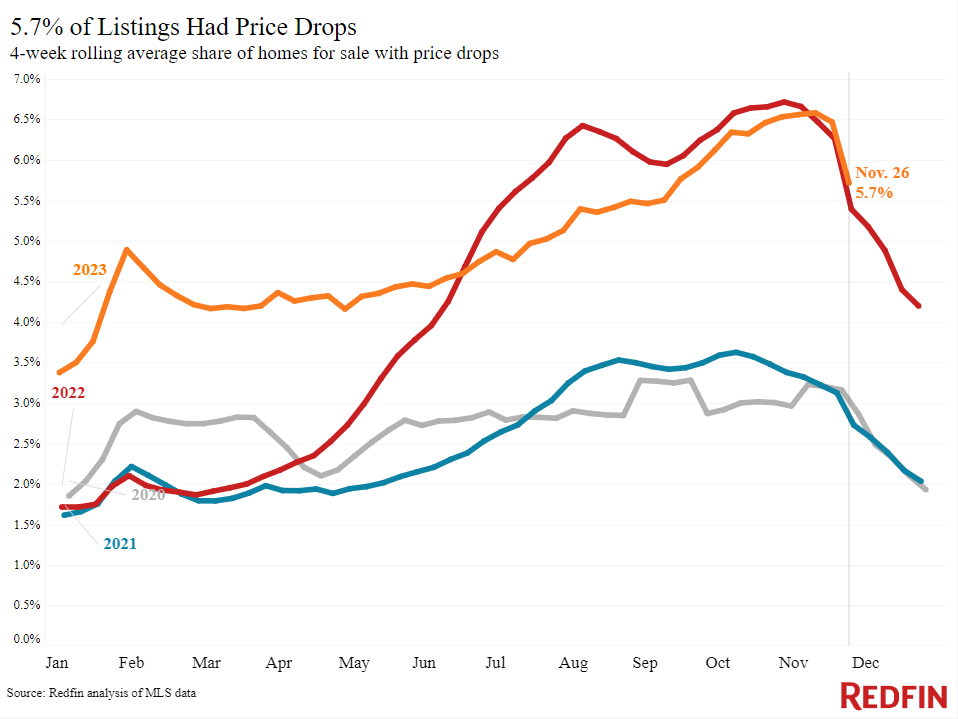

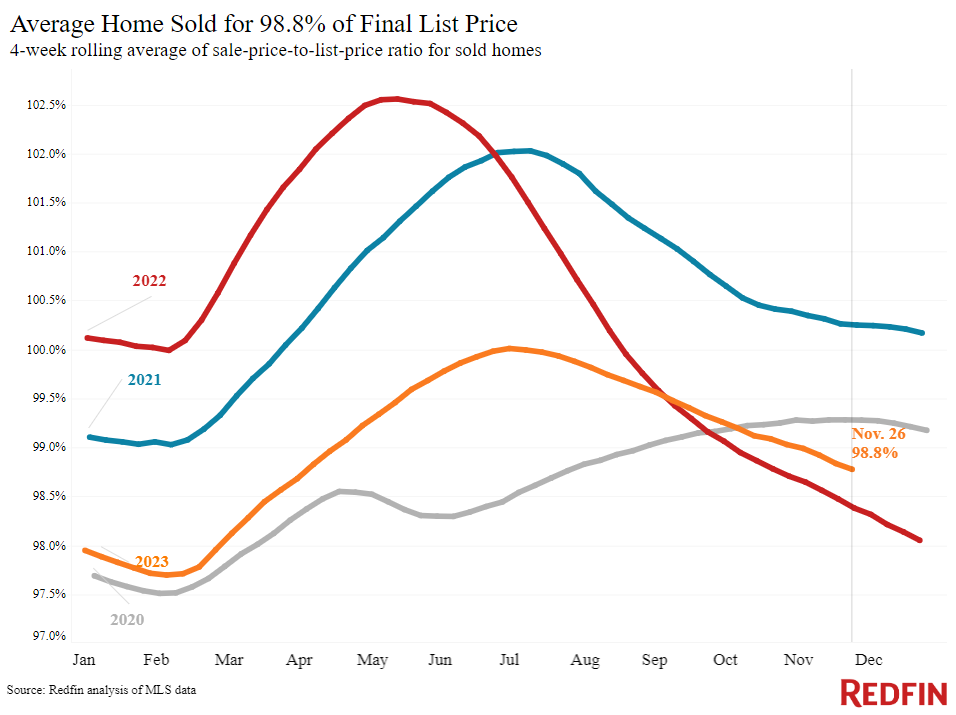

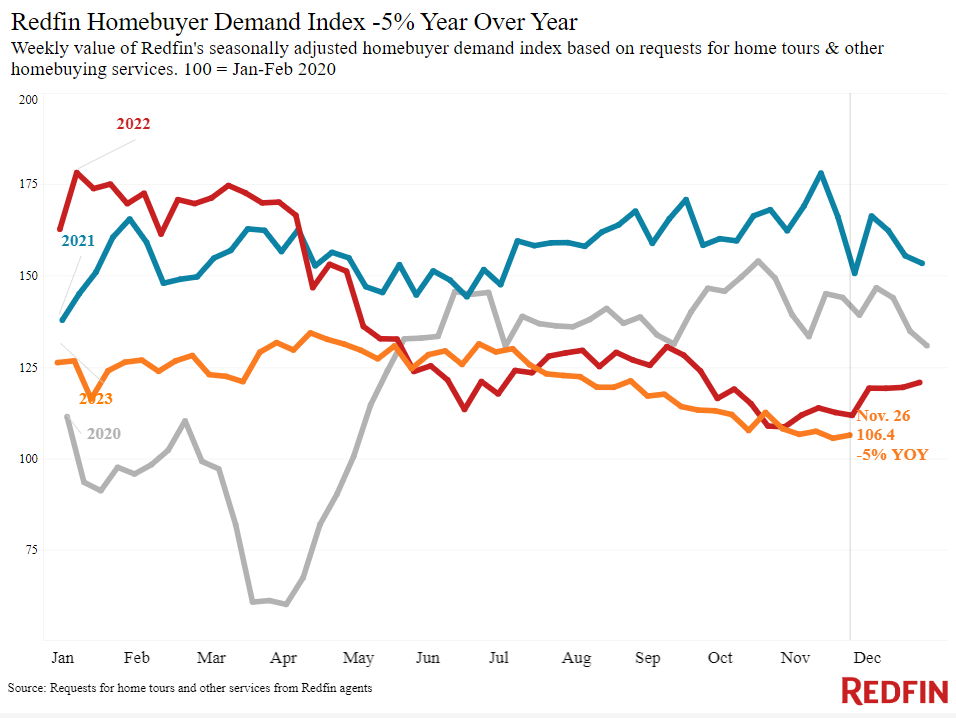

Monthly payments are falling from their peak because mortgage rates are falling from their peak. The weekly average 30-year mortgage rate is 7.29%, down from a high of 7.79% in October, and the daily average is 7.13% as of November 29, its lowest level since the start of September. Rates have declined enough to offset rising home prices; the median sale price is up 4%. Prices are up because inventory is low; the total number of homes for sale is down 7% year over year. But there is hope for buyers wanting more homes to choose from: New listings are up 6%, the biggest uptick in over two years. Buyers are taking note of slightly improved conditions: Mortgage-purchase applications are up 5% week over week.

“Mortgage rates are dropping due to easing inflation and investors betting the Fed will cut interest rates sooner than expected,” said Redfin Economics Research Lead Chen Zhao. “Declining rates, along with a sizable year-over-year increase in new listings, are leading to more favorable conditions for some buyers. My advice for serious homebuyers is to compare housing costs to recent highs instead of long-ago lows. Housing costs are at their lowest level in three months and it’s unlikely they will drop significantly anytime soon. That makes it a relatively good time to lock in a rate.”

Refer to our metrics definition page for explanations of all the metrics used in this report.