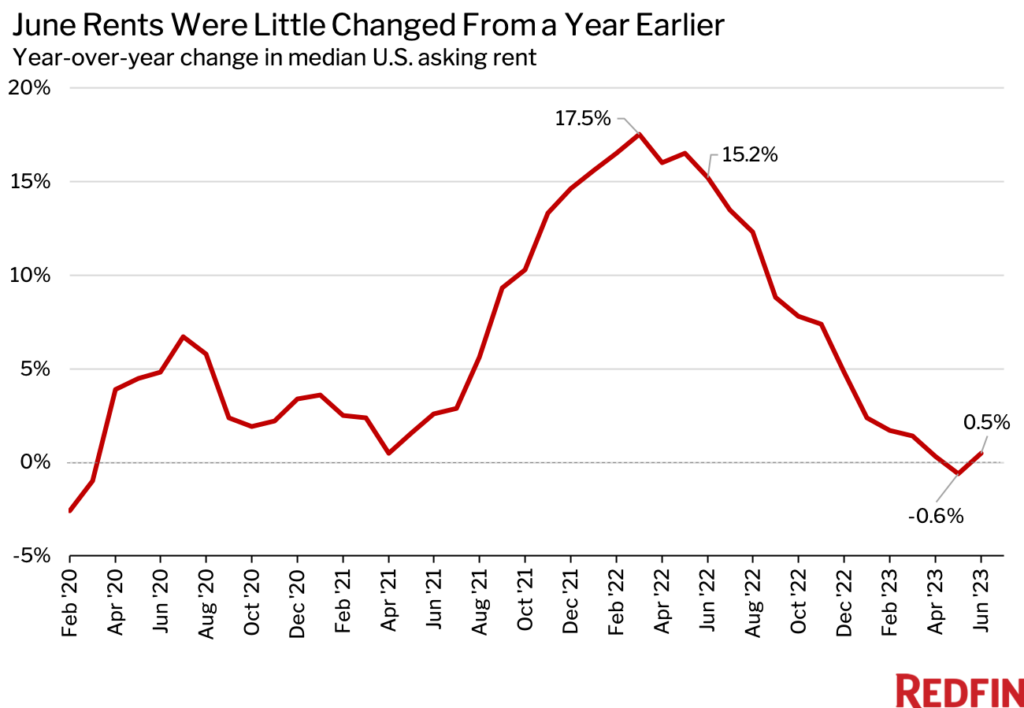

The U.S. rental market has been slowing for more than a year, but the median asking rent is still only $24 below its record high. It was $2,029 in June, little changed from $1,995 one month earlier, $2,019 one year earlier and a record high of $2,053 set in August 2022.

In percentage terms, rents were up 0.5% year over year in June, not far from May’s 0.6% annual drop. Rents rose 1.7% from one month earlier in June.

“The housing market tends to be ‘downside sticky,’ which means rents don’t typically fall much even when renter demand pulls back,” Redfin Deputy Chief Economist Taylor Marr said. “Instead of lowering rents when business is slow, many landlords offer perks like a free month’s rent or discounted parking, which tends to be less of a hit to profits.”

Marr continued: “The steep slowdown in rent growth over the last year is providing some relief for renters, who now have more room to negotiate as their landlords grapple with rising vacancies. But with rents near their record high, most renters still aren’t finding big bargains.”

While the dropoff in rent growth hasn’t made a big dent for many renters, it has helped ease the historic inflation plaguing U.S. consumers, according to data released today. Consumer prices were up 3% this year through June, a deceleration from the 4% figure reported in May and the peak of about 9% last summer. The cost of shelter, which mainly includes rent, rose 0.4% from a month earlier in June on a seasonally adjusted basis—a significant cooling from 0.8% at the end of last year. Inflation data typically lags Redfin’s rental data, so the slowdown in inflation reported today is in large part due to the deceleration in rent growth over the past year.

“Inflation should continue easing this year and into 2024, partly because the recent slowdown in rent growth isn’t fully baked into inflation data yet, and partly because rents have room to fall,” said Redfin Economics Research Lead Chen Zhao. “Rents have room to come down because there remains a backlog of under-construction rentals that have yet to hit the market, which means landlords will continue grappling with vacancies and won’t be able to hike rents as rapidly.”

Rent growth has cooled from its 2022 high partly because fewer people are moving due to economic uncertainty and slowing household formation, and partly because the number of options renters can choose from has surged. Completed residential projects in buildings with five or more units rose 23.9% year over year to 493,000 on a seasonally adjusted basis in May—the most recent month for which data is available—which means landlords have more vacancies to fill and less leeway to raise prices.

While a homebuilding boom has led to more rentals on the market, the boom is easing. The number of permitted residential projects in buildings with five or more units fell 12.2% year over year to 540,000 on a seasonally-adjusted basis in May. Permits, or approvals given by local jurisdictions to start construction projects, are a leading indicator of what’s happening in the housing market. Completions are a lagging indicator.

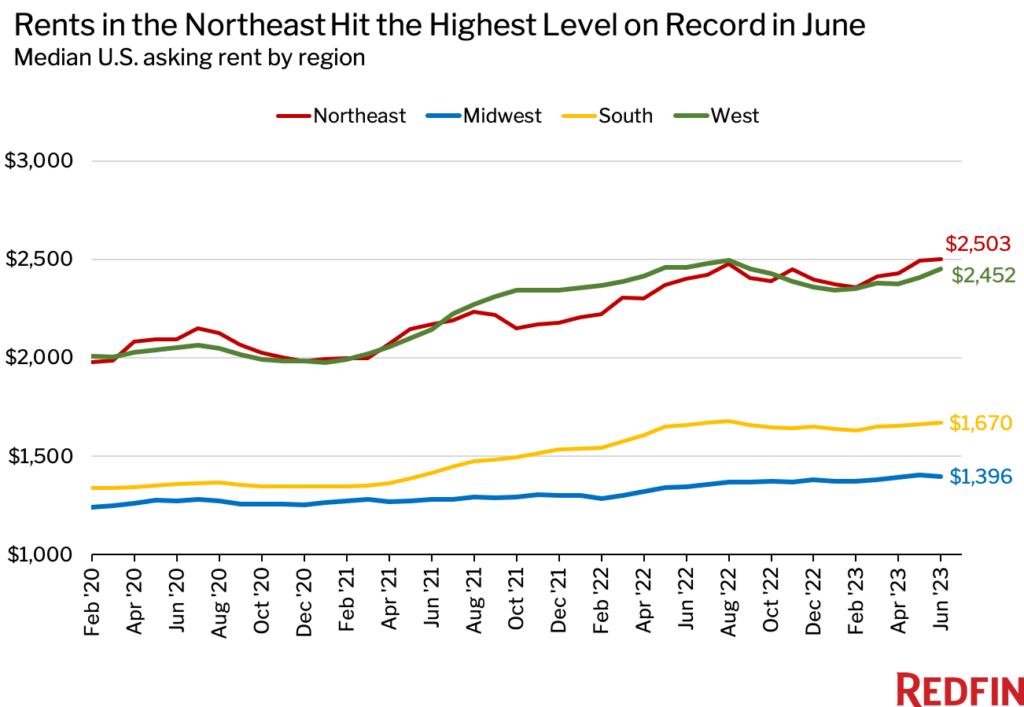

In the Northeast, the median asking rent rose 4.3% year over year to a record $2,503 in June. By comparison, asking rents rose 3.7% to $1,396 in the Midwest, 0.8% to $1,670 in the South, and fell 0.3% to $2,452 in the West. While rents continued climbing across much of the U.S., rent growth was far below its peak in most of the country.

Rent growth has been slowing fastest in the West and South in part because it accelerated so quickly during the pandemic as people flooded into Sun Belt cities including Phoenix, Miami and Dallas. Now, rents in those regions have more room to cool as supply catches up with demand.

But while rents have dipped from a year ago in some areas, affordable deals are still often hard to come by.

“The headlines say San Francisco’s housing market is plummeting, but I’m still seeing people moving in and spending $4,000 a month on rent,” said local Redfin Premier real estate agent Ali Mafi. “A lot of tech workers who left the Bay Area for places like Austin during the pandemic are now coming back because their employers cut their pay when they moved and/or have asked them to come back to the office.”

Asking price data includes single-family homes, multi-family units, condos/co-ops and townhouses from Rent.com and Redfin.com.

Redfin has removed metro-level data from monthly rental reports for the time being as it works to expand its rental analysis.

Prices reflect the current costs of new leases during each time period. In other words, the amount shown as the median rent is not the median of what all renters are paying, but the median asking price of apartments that were available for new renters during the report month.