The U.S. is confronting what is likely to be the deadliest week so far in the coronavirus outbreak and with over 10 million new unemployment claims over the past two weeks the backdrop for the housing market is fairly bleak.

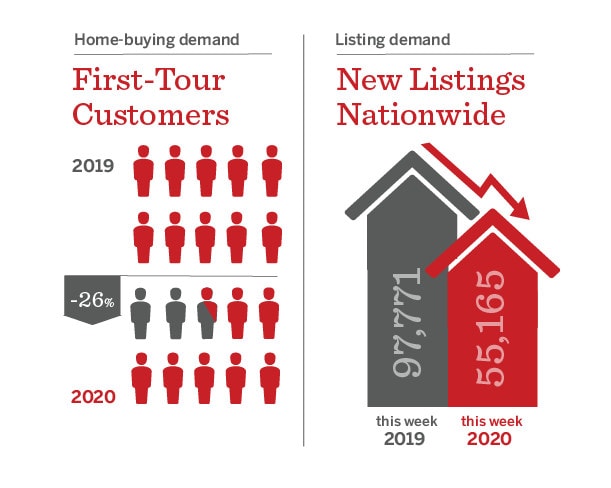

Yet somehow the stability in home-buying demand we saw last week has extended into this week. We measure home-buying demand by the annual growth rate in customers going on their first tour with a Redfin agent. For the seven days ending April 7, home-buying demand was down 26% compared to the prior year. When we reported on this number last week, it was down 33% compared to the prior year. The majority of the improvement from last week is a result of Redfin routing a larger share of customer inquiries from Redfin.com to our own agents, referring fewer inquiries to our partner agents.

The recent stability is encouraging after several weeks of free-falling home-buying demand; in January and February Redfin’s home-buying demand was up 27% compared to the prior year.

“The resilience in home-buying demand may be driven by the recent rally in the stock market which gained 20% since it bottomed out on March 23, by low mortgage rates which are now back below 3.5%, or by the simple lure of getting a deal,” said Redfin lead economist Taylor Marr. “But until we see a sustained national slowdown in new COVID-19 infections, hospital admissions, and deaths, it’s too soon to say if we’ve reached the bottom for home-buying demand.”

Personal Safety Concerns Accelerate the Move to a Virtual World

Getting access to a property for in-person showings is getting increasingly complicated as buyers, sellers, and agents all increase safety precautions. Miriam Westberg, a Redfin agent in San Francisco said, “Every house is now like a luxury listing. Buyers need to be pre-approved with a reputable lender and most listing agents will ask 20 questions to see how serious they are before they can walk through the door.” Sellers are leaving cabinets and closets open for a touchless tour, agents are donning gloves and masks, and in California prospective buyers have to sign a form certifying that they don’t have coronavirus.

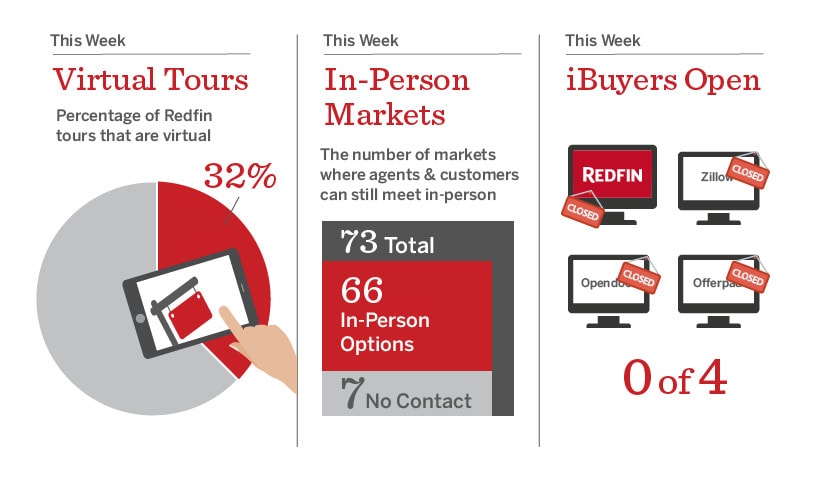

More and more, buyers are opting to tour the home remotely via video chat with either their agent, the seller, or sometimes even a tenant broadcasting the interior of the house back to the buyers’ living room. Last weekend 32% of Redfin tour requests were for video-chat tours, up slightly from 30% of tour requests the prior weekend.

On April 2, we made it easier for prospective buyers to view Redfin listings online, highlighting our virtual walkthroughs front and center on Redfin.com. The number of daily clicks on our virtual walkthroughs have more than doubled since we updated our site.

For buyers who want a real-time showing, but aren’t ready to schedule a private showing, we’ve moved the open house online, as well. Last weekend we live-streamed 10 open houses with buyers directing the listing agent which rooms to visit by text chat. This is a tiny fraction of the homes Redfin has for sale, but just a few weeks ago video-chat tours were only .2% of our tour requests.

Most Sellers Are Sitting This Spring Out

Nationwide, new listings are down 44% compared to the prior year for the seven days ending April 3. That’s a significant pullback compared to the 33% decline we reported last week and there’s no indication this trend will reverse anytime soon.

The big question is whether sellers will be able to wait until stay-at-home orders are lifted. Redfin agents report that many sellers want to list in early to mid-May, but it’s still unclear whether the orders will be lifted by then. Some sellers may not be able to wait any longer if they’ve already moved or their family simply doesn’t fit in their old home anymore.

But some sellers are pressing forward despite the stay-at-home restrictions. Sylva Khaylian, a Redfin agent in Los Angeles reported that a lot of her sellers are worried prices will be lower later and just want to get on with it. We interviewed 16 Redfin clients this past week and only one-third of them felt confident about their sale. Clients with homes in affordable or highly desirable neighborhoods still felt the market was in their favor.

Sales Down, Prices Flat

With fewer homes to choose from, pending U.S. home sales are down 49% in the seven days ending April 3. Now we’re getting our first view into closed sales since the pandemic began, which were only down 13% for the seven-day period ending March 28. We expect the weakness in pending sales to spread to closed sales as April progresses.

It’s still a little too soon to look at the impact of the pandemic on sale prices, but the median price for new listings has fallen to $309,000 from $330,000 earlier this year. Median listing prices are now flat with last year after being up nearly 8% at the peak in early March. Some of the price decline is due to a bigger slowdown in the luxury market, with homes above $750,000 only representing 8% of new listings since mid-March compared to 9% in the prior year.

Surprisingly, we’re still not seeing an increase in price reductions compared to the same time last year. Rather than reducing the price, sellers may be pulling their homes off the market to wait for a better time. Sellers were twice as likely to withdraw from the market in the seven days ending April 3 as they were at the same time last year.

A New Kind of Bidding War

Despite the decline in pending sales, the combination of fewer new listings and more sellers backing out of the market means that the number of homes for sale is now down 19% compared to last year. When we reported this last week it was down 17%.

MaryDell Penney, the Redfin Market Manager in North Florida said the market for affordable homes continues to be competitive, attributing the strength in that segment of the market to low interest rates. Competition for affordable homes is a sentiment we heard echoed by Redfin agents across the country.

But the bidding wars aren’t the 10-offer, $50,000 dollars-over-list-price battle royales we saw earlier in the year. Leslie White, a Redfin agent in Washington D.C., said an offer at list price and a personal letter to the seller was good enough to beat out two other buyers. Her buyers had included an escalation clause to automatically increase the price of their offer if another offer came in at a higher price, but they didn’t need to use it.

Keep an Eye on the Mortgage Market

Rates for a 30-year mortgage have dropped back to 3.4% as of April 6, but there has been a disturbance in the mortgage force. Some lenders have stopped making jumbo loans for high-priced homes, citing a substantial decline in investors willing to purchase those loans. The big banks like Wells Fargo are still making jumbo loans, but now require 20% down-payments.

At the other end of the market, many lenders have also stopped originating Federal Housing Administration (FHA) loans. FHA loans are often used by first-time homebuyers because they let buyers put as little as 3.5% down and are more lenient for borrowers with lower credit scores. Lenders and government regulators alike have started to worry that an increasing percentage of first-time buyers may not be able to make their monthly payments as the economy continues to stagger under the weight of the coronavirus.

That’s it for this week. Please stay safe, and if you can, stay home. If you’re out on the front lines, please accept the most sincere thanks from everyone here at Redfin.

Redfin is publishing this housing-market update as a way to inform our customers, not our investors. Even though we’re notifying investors through a government filing about this customer update, we’re not updating, withdrawing, or affirming the first quarter financial guidance we issued on February 12, 2020. Unless otherwise noted, all data in this update is as of April 8, 2020.

Surprising Resilience in Home-Buying Demand Despite Job Losses and Coronavirus Spread

- BY System Admin

- DATE 26/11/2024